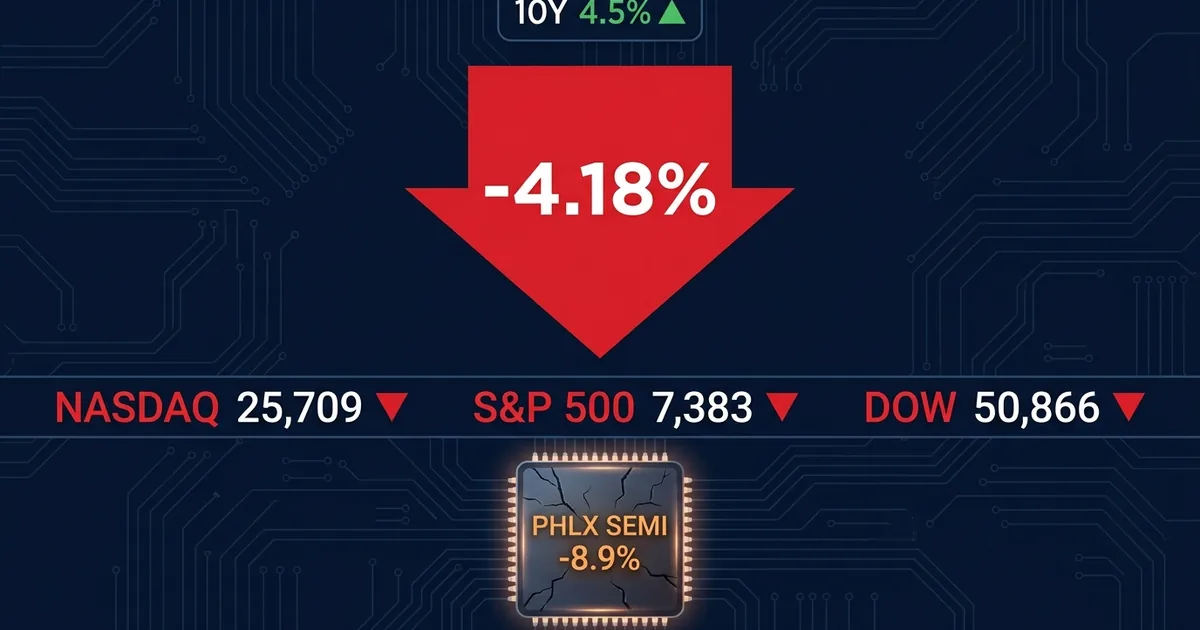

The Nasdaq plunged 4.18% on Friday, its steepest single-session drop since April 2025, as a stronger-than-expected May employment report collided with a two-day semiconductor rout to produce the ugliest trading day of the year. The convergence of sticky labor-market strength and evaporating AI chip optimism did exactly what neither catalyst could have done alone: it forced a wholesale repricing of when, or whether, the Federal Reserve will cut rates this cycle.

The Numbers Tell the Story

The S&P 500 shed 2.64% to close at 7,383.74, while the Dow Jones Industrial Average lost 695 points, or 1.35%, settling at 50,866.78. But the real carnage was concentrated in chips. The Philadelphia Semiconductor Index cratered as much as 8.92% intraday, with CNBC reporting that Micron Technology dropped 17% over just two sessions, Intel fell 9%, and AMD slid 12.6%. Broadcom, which kicked off the selloff with a Tuesday evening earnings miss, closed down 12.59% for the week after its third-quarter AI semiconductor revenue guidance of $16 billion landed below the $17.2 billion Wall Street had penciled in.

A Jobs Report That Changed the Math

The Bureau of Labor Statistics reported that nonfarm payrolls surged by 172,000 in May, more than double the 80,000 consensus estimate compiled by Dow Jones. Unemployment held at 4.3%, and April’s figure was revised upward to 179,000. Leisure and hospitality led with 70,000 new positions, a figure five times the sector’s recent monthly average, likely boosted by World Cup preparation hiring. Local government added 55,000, and healthcare contributed 35,000.

The reaction in rates was immediate. The 10-year Treasury yield jumped above 4.5%, and the 30-year pushed past 5%, according to CNN. Traders slashed expectations for near-term Fed rate cuts, with some now pricing in the possibility of a hike before year-end. Just weeks ago, the market was still betting on at least one cut by September, a narrative that evaporated in a single Friday morning.

Why This Selloff Is Different

Most 2026 pullbacks have been geopolitical, driven by oil spikes or trade policy shocks. This one is structural. The economy came in too strong at exactly the moment the AI trade’s momentum broke.

Broadcom’s guidance miss was not a disaster in isolation. The company still projected 200% year-over-year AI chip revenue growth. But with semiconductor stocks priced for perfection after a multi-year run, merely meeting high expectations was no longer enough. The announcement that Broadcom would shift to a “chips only” model, dropping integrated AI systems from its roadmap, rattled investors who had been betting on higher-margin bundled offerings.

The macro backdrop made it worse. When Treasury yields are falling, growth stocks absorb bad news. When yields are surging because the labor market refuses to cool, there is nowhere to hide. The strong jobs data, particularly the breadth across sectors and the upward revision to April, suggests the economy is running hotter than the Fed’s models assumed heading into summer.

What the Fed Is Watching

Fed Chair Kevin Warsh has been clear: the committee needs sustained evidence of cooling before moving on rates. Friday’s report delivered the opposite. Average monthly private payroll growth in the first quarter of 2026 was already running at 2.5 times the 2025 average. The prime-age labor force participation rate ticked up to 83.9%, above the pre-pandemic peak. These are not the numbers of an economy that needs monetary easing.

The futures market now reflects a roughly 30% probability of no cuts at all in 2026, up from below 10% just a week ago. If June’s Consumer Price Index comes in hot, that number could climb further.

The Broader Signal

Friday’s selloff marks a potential inflection point for 2026. The first half of the year was dominated by the AI infrastructure trade and a series of record closes. Now the market faces a scenario where strong growth sustains inflation, keeping rates elevated, while the AI hardware cycle shows its first signs of deceleration. That is not a crisis. But it is a repricing, and those tend to be messier than the rallies that precede them.

The question heading into next week is whether this is a one-day flush or the start of a rotation. With Yahoo Finance reporting that the jobs data has effectively killed any remaining hope for a summer rate cut, the answer may depend less on earnings and more on what the bond market does next.