The US economy delivered a contradiction on Thursday that the Federal Reserve cannot easily resolve. First-quarter growth was revised down to a 1.6% annual rate, weaker than the 2.0% first reported, while the Fed’s preferred inflation gauge ran hot at 3.8%. Slower growth and stickier prices arriving on the same morning is the textbook setup the central bank spends its life trying to avoid, and it lands with equities sitting at record highs that may be pricing in a rate path the data no longer supports.

Two Numbers Moving in the Wrong Directions

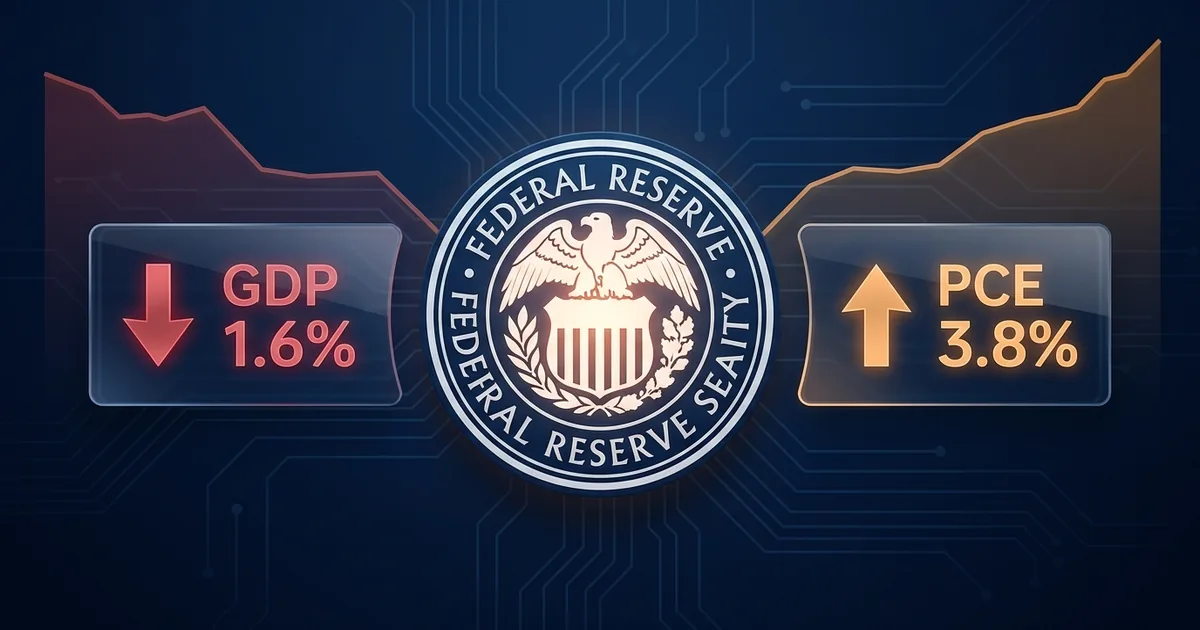

Start with growth. The Bureau of Economic Analysis cut its estimate of first-quarter GDP to 1.6%, down four-tenths of a point from the advance reading, with the revision driven by softer business investment and weaker consumer spending. The downgrade is detailed in the agency’s second-estimate release, and the composition matters more than the headline: when the cut comes from investment and consumption, the two engines that actually drive durable expansion, it signals a real loss of momentum rather than a statistical quirk.

Now inflation. The personal consumption expenditures index, the measure the Fed weighs most heavily, came in at 3.8%, well above the 2% target and the firmest reading in years, as laid out in the combined PCE and GDP data. Inflation running near double the target while growth slows is the precise combination that has no clean policy answer.

Why This Boxes In the Fed

Here is the trap, stated plainly. The Fed has two tools and they point in opposite directions. If it cuts rates to support a slowing economy, it risks pouring fuel on inflation that is already running hot. If it holds or hikes to crush inflation, it risks tipping an economy growing at just 1.6% toward stall speed. There is no move that addresses both problems at once. Every option helps one number and hurts the other.

This is why the week’s data complicates the June meeting so badly. Markets had largely penciled in a Fed leaning toward easing. A 3.8% inflation print makes a cut much harder to justify with a straight face, a tension we flagged when April’s CPI landed and the case for a June hold firmed up, covered in our breakdown of April inflation and the June rate decision. The new data pushes the same direction, only harder.

The Word Nobody at the Fed Wants to Say

There is a term for slow growth paired with high inflation, and it is the one central bankers dread: stagflation. We are not there in full, 1.6% growth is sluggish, not contracting, and the labor market has not broken. But the direction of travel is unmistakable, and the early labor signals are softening too, with initial jobless claims edging up to their highest level in over a month.

Stagflation is uniquely dangerous because the standard playbook fails. In a normal slowdown, the Fed cuts and inflation stays tame, so easing is a free lunch. In a stagflationary slowdown, easing reignites prices and tightening deepens the downturn. The policy that fixes one problem worsens the other, which is exactly why the 1970s version took years and a brutal recession to break.

The Market Is Not Listening, Yet

The strangest part of Thursday is what the stock market did with this news: very little. Equities held near records, propelled by AI-driven earnings optimism and easing geopolitical tension rather than the macro data. That disconnect is the real risk. When growth is slowing, inflation is sticky, and the Fed’s hands are tied, a market priced for a smooth path of rate cuts is a market priced for a scenario the data is actively undermining.

None of this means a sell-off is imminent. Records can persist longer than the fundamentals seem to warrant, especially when a handful of mega-cap AI names are doing the heavy lifting. But the gap between what the economic data is signaling and what the equity market is pricing has widened, and gaps like that tend to close in one direction.

The Bigger Read

Thursday’s reports reframe the central question for the back half of the year. It is no longer whether the Fed cuts, it is whether the Fed can cut without making inflation worse, and the answer just got murkier. Growth at 1.6% argues for support. Inflation at 3.8% argues against it. The central bank is caught between its two mandates with no costless move available.

Watch the June meeting and the language around it, not just the rate decision itself. If the Fed signals it is willing to tolerate above-target inflation to protect growth, that is one regime. If it signals price stability comes first even at the cost of the expansion, that is another. The data just made that choice unavoidable, and the market has not fully reckoned with either answer.