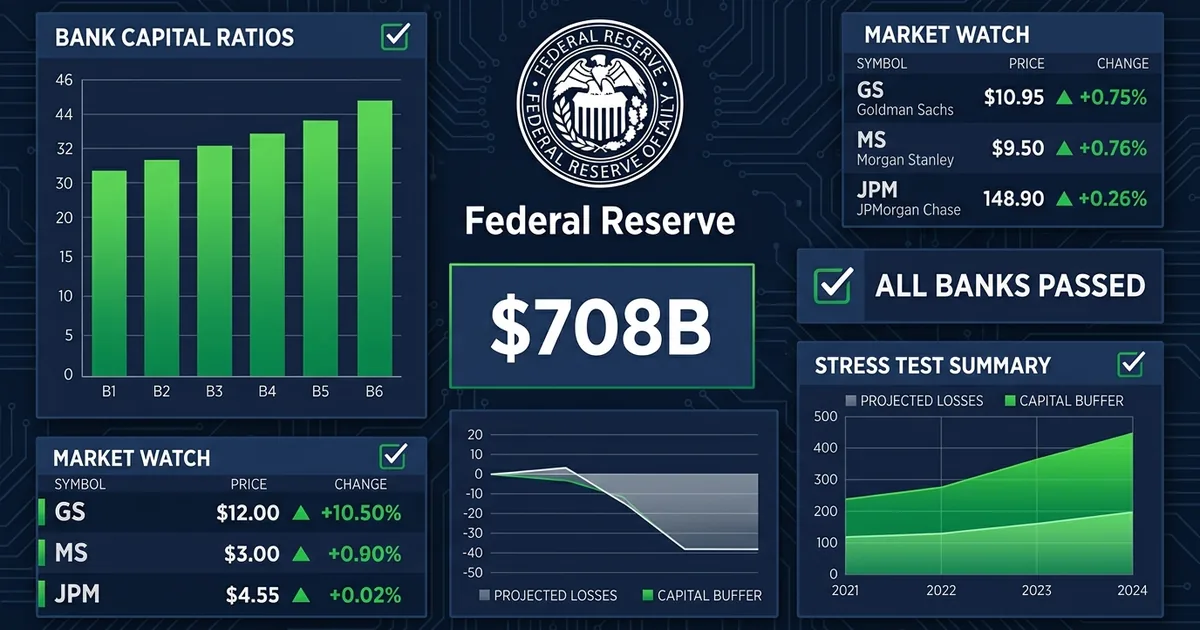

The Federal Reserve’s annual stress test delivered the verdict Wall Street wanted: all 32 of the nation’s largest banks survived a hypothetical recession that would wipe out more than $708 billion in loans and investments. Within hours of the results dropping on June 24, Goldman Sachs hiked its dividend 11 percent and Morgan Stanley authorized a fresh $20 billion buyback program. The capital return floodgates are open, and the banks are not waiting around.

The Doomsday Scenario That Nobody Failed

The Fed’s “severely adverse” scenario reads like a financial horror film. Unemployment hits 10 percent. Home prices crater 30 percent. Commercial real estate collapses by 39 percent. Stock markets lose 58 percent of their value. Under those conditions, the 32 tested banks would collectively absorb approximately $708 billion in losses, according to the Federal Reserve’s official results, with their aggregate common equity tier 1 capital ratio falling from 12.8 percent to 11.2 percent.

That 11.2 percent floor matters because it sits well above the regulatory minimum. Every single bank cleared the bar, which means none faces a forced capital raise or a dividend cut. The loss breakdown tells you where the stress concentrates: roughly $200 billion in credit card losses, $160 billion in commercial and industrial loan write-downs, and $75 billion in commercial real estate impairments.

Goldman, Morgan Stanley, and the Payout Race

The market reaction was swift. Goldman Sachs bumped its quarterly dividend to $5.00 per share, an 11 percent increase that reflects the bank’s confidence in its capital cushion. Morgan Stanley went further, raising its payout 15 percent to $1.15 per share and reauthorizing a multi-year stock buyback program worth $20 billion. Both moves signal that the biggest names on Wall Street see the stress test results as a green light to return cash rather than hoard it.

This is where the story gets interesting for investors. The stress test is supposed to be a constraint on capital distribution. When every bank passes comfortably, that constraint disappears, and the competitive pressure to reward shareholders takes over. Expect more dividend hikes and buyback announcements from JPMorgan, Bank of America, and the regional banking giants in the coming weeks, now that the stress test has confirmed sector-wide resilience.

The Frozen Buffer Problem

There is a twist that makes the 2026 results unusual. The Fed announced in February that it would freeze stress capital buffer requirements at 2025 levels until 2027, pending a comprehensive review of its testing methodology. That means the 2026 results carry no immediate consequence for required capital levels. Banks are being tested but not adjusted.

The freeze was a concession to industry complaints that the stress test models were outdated, overly punitive in some areas and too lenient in others. The banking lobby had argued for years that the models failed to capture how modern banks actually manage risk, particularly in areas like derivatives hedging and AI-driven credit underwriting. The Fed agreed to pause and rethink, which is exactly the kind of regulatory breathing room that makes bank CFOs sleep easier.

But the freeze also raises a legitimate question: if the test results do not change capital requirements, what exactly is the test doing? The answer, for now, is providing a public confidence signal. The $708 billion loss absorption number is headline-ready reassurance for a post-SVB world still nervous about bank fragility. Whether it is a meaningful regulatory tool in 2026, or just a well-produced annual ritual, depends on what the Fed does when the freeze lifts.

Credit Cards Are the Weak Spot

Buried in the aggregate numbers is a warning sign worth watching. The $200 billion in projected credit card losses represents the single largest category of stress losses, and it maps onto a real-world trend that has been building for over a year. Credit card delinquency rates have been climbing since late 2025, driven by stubborn inflation, rising minimum payments, and a consumer base that loaded up on revolving debt during the post-pandemic spending boom.

The banks will tell you their underwriting standards have tightened. The data says delinquencies are still rising. The stress test says the system can absorb the hit. All three things can be true at the same time, but only one of them keeps a Fed already navigating a complex inflation picture up at night.

What Comes Next

The real test for the banking sector is not the annual Fed exercise. It is the economic environment that unfolds over the next 12 months. Inflation hit a three-year high on a key measure this week. Commercial real estate vacancy rates remain elevated in major metros. The geopolitical backdrop, from Middle East energy supply disruptions to the escalating U.S.-China technology standoff, introduces tail risks that no stress model can fully capture.

For now, the market is focused on the easy story: banks passed, dividends are going up, buybacks are coming. The harder story is whether the capital cushions that look comfortable today will still look comfortable if two or three of the Fed’s hypothetical stressors start showing up in the real economy at the same time. The 2026 stress test says the system is ready. History says the system always looks ready right up until the moment it is not.