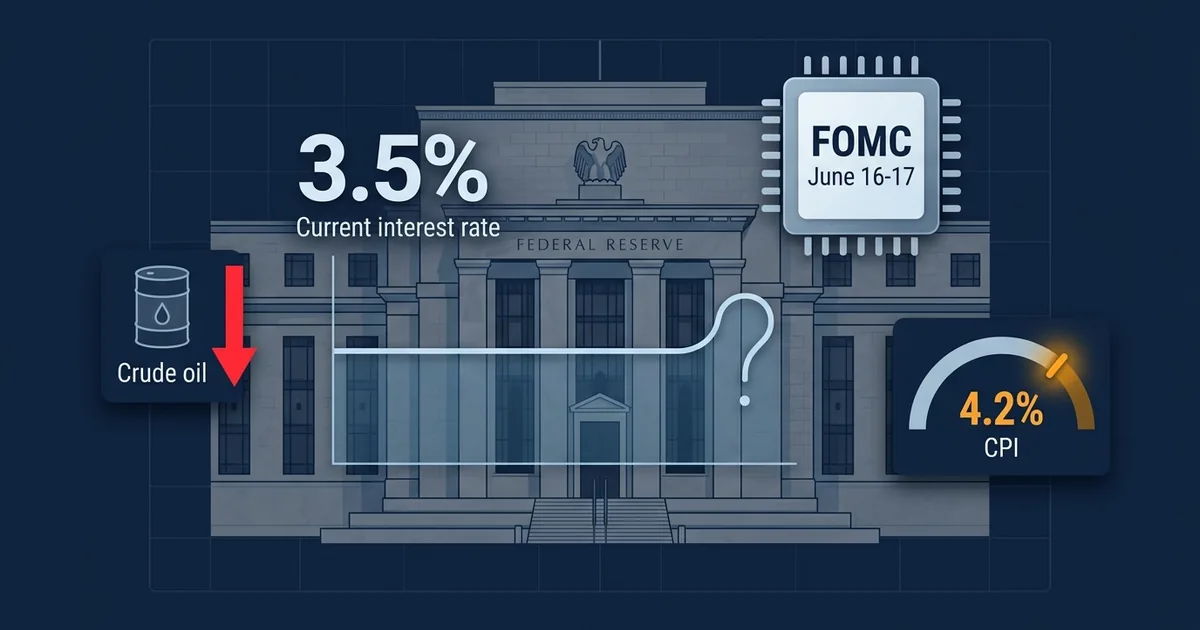

The Federal Reserve two-day policy meeting opens Tuesday with interest rates at 3.5% to 3.75% and a near-unanimous market expectation of no change. But the backdrop has shifted dramatically in the 72 hours since oil prices cratered on the US-Iran peace deal, giving policymakers an inflation variable they did not have when they prepared their staff forecasts.

The Setup: Hold at 3.5%, but the Tone Matters

Markets are pricing a 99.6% probability that the FOMC holds rates steady at the conclusion of Wednesday meeting, according to Polymarket tracking. That consensus has been locked in for weeks, and nothing in Friday data changed it. The real question is not the rate decision itself but the language in the post-meeting statement and Chair Jerome Powell press conference.

Before this weekend, the Fed calculus was straightforward: May CPI came in at 4.2%, its highest level in three years, driven almost entirely by energy costs. The jobs market remained resilient, consumer spending held up, and there was no obvious reason to cut. The June meeting was shaping up as a hold-and-wait affair, with the statement likely reiterating data dependence and inflation vigilance.

Oil Changes the Math

Then the Iran deal happened. WTI crude crashed through 0 on Monday morning for the first time in three months. Brent dropped more than 4% to around 3. If the Strait of Hormuz reopens as planned and Iranian oil exports resume, the energy component that drove CPI to 4.2% could reverse course over the next two to three months.

The Fed will not react to a single weekend of oil price moves, and nobody expects them to signal a cut this week. But the shift in the energy outlook gives the committee room to soften its inflation language. A move from “inflation remains elevated” to something acknowledging that “recent developments in energy markets may ease price pressures” would be a meaningful dovish signal, even without a rate change.

What the Bond Market Is Already Pricing

The 10-year Treasury yield pulled back from the 5.1% level it hit in May, reflecting the market rapid repricing of inflation expectations. If the Fed dot plot, which projects each member rate path, shifts even modestly toward a September or December cut, expect a sharp rally in duration-sensitive assets: growth stocks, REITs, and long-dated bonds.

Conversely, if Powell strikes a hawkish tone, emphasizing that one weekend of geopolitical news does not change the structural inflation picture, the “higher for longer” trade reasserts itself. In that scenario, the recent tech rally could give back gains quickly.

The ECB Complication

The Fed is not operating in isolation. The European Central Bank hiked rates to 2.25% last week, its first increase since 2023, citing energy-driven inflation that is now potentially receding. A scenario where the ECB just hiked and the Fed starts signaling cuts would widen the transatlantic rate differential and strengthen the dollar, complicating the picture for multinationals and emerging markets.

What to Watch Wednesday

Three things matter more than the rate decision itself. First, the dot plot: any shift in the median 2026 rate projection below 3.5% would be dovish. Second, the statement language on inflation: does the committee acknowledge the changed energy backdrop or stick to its prior framing? Third, Powell press conference: how he characterizes the Iran deal potential impact on the inflation outlook will set the tone for the next six weeks of trading.

The hold itself is already priced. Everything that matters is in the margins.