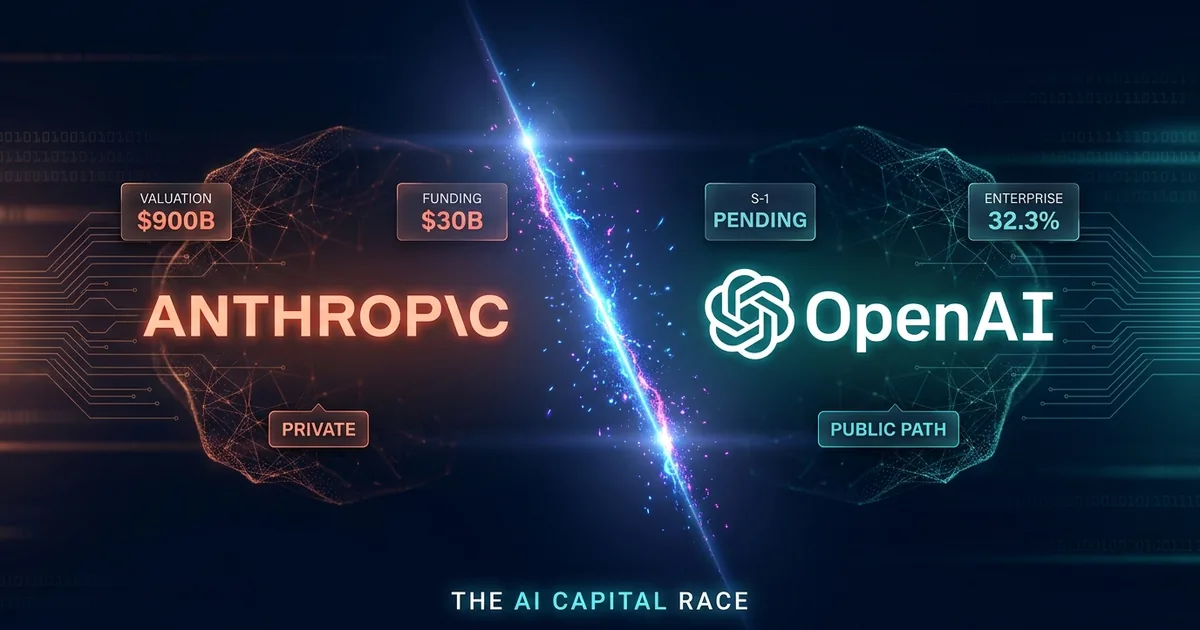

Anthropic is back in the market. This time it is for $30 billion at a $900 billion pre-money valuation, with the round expected to close by the end of May, according to reporting that first surfaced in Bloomberg last Tuesday. Greenoaks, Sequoia, Altimeter, and Dragoneer are each tipped to write checks of $2 billion or more. If the paperwork clears the way the deal team is moving, Anthropic will sit at a higher private valuation than OpenAI roughly three months before OpenAI is expected to file its S-1.

The capital story is no longer a sideshow. It is the only story.

The Math Versus February

Three months ago, Anthropic was a $380 billion company on paper. The new round nearly triples that mark, and it does so without a single new commercial milestone disclosed publicly. What changed is what the market saw in the data. Ramp’s April AI Index, the spend tracker that has become the closest thing the enterprise AI economy has to a Nielsen rating, put Anthropic at 34.4 percent enterprise share to OpenAI’s 32.3 percent. That was the first time the line crossed.

Inside the room, the round is being framed as the closing argument for a thesis that has been building since the Series G in February. Claude Code, the agentic coding product launched into full general availability in February 2026, is the highest-revenue AI product in the enterprise outside of OpenAI’s flagship subscription. The Goldman Sachs deployment alone, which became public via the May 4 joint-venture announcement with Blackstone and Hellman & Friedman, is reportedly running at a nine-figure annual rate. That is not the run-rate Wall Street modeled going into the year.

Compute, Compute, Compute

What does Anthropic actually do with another $30 billion? The same thing every frontier lab does. It buys compute and then it buys more compute. The xAI deal that closed earlier this month, in which Anthropic took down all the compute capacity at Elon Musk’s Colossus 1 data center in Tennessee, was a structural admission that Claude’s training and inference roadmap is fully bottlenecked by chip access. Even with Google’s $10 billion at a $350 billion valuation from late last year, plus the additional $30 billion in performance-gated tranches Google has committed, Anthropic is still rationing inference capacity for its highest-revenue enterprise customers.

The new round funds the Vera Rubin orderbook through 2027 and locks in the data-center power contracts in Arizona, Virginia, and Tennessee. That is the only durable moat in this market. Whoever can spend $30 billion on compute by Christmas, and another $40 billion next year, is in the conversation. Whoever cannot is not.

OpenAI’s IPO Clock Is Ticking Faster Than Anthropic’s Cap Table

Here is the structural problem for OpenAI. CFO Sarah Friar’s reported preference to slip the IPO from late 2026 into 2027 hit the wires last week, alongside a $25 billion revenue, $14 billion loss disclosure that did not help the comp set. The longer OpenAI sits private and burns, the more capital Anthropic can stack at a higher mark. The longer Anthropic sits private at a higher mark, the more questions get asked about the IPO valuation OpenAI eventually files.

According to CNBC’s reporting, Anthropic’s deal team has kept the cap table tight on this round, with the four named anchors expected to absorb roughly $8 billion of the $30 billion target between them. The remainder is going to a small group of sovereign and pension funds that did not get into the February Series G at $380 billion. The Saudi Public Investment Fund and Singapore’s GIC are both confirmed names on the road show, according to people familiar with the talks.

The implication is precise. Anthropic is not optimizing for valuation. It is optimizing for runway and signaling. A $900 billion private mark is the maximum credibility Anthropic can hold without being public, and it is the exact number that resets the OpenAI IPO comp.

Where The Risk Sits

Three things could go sideways. The first is the FTC. Lina Khan’s successor at the agency has signaled an interest in AI joint ventures and the cross-equity structures that link foundation models to cloud providers. Google’s existing $40 billion-plus position in Anthropic is the most likely target for a “second look” review if the deal closes at this scale. Inside the building, Anthropic’s general counsel has spent the past four weeks walking through the Section 7 implications with outside counsel at Sullivan and Cromwell.

The second risk is the macro frame. The bond market is in revolt, with the 30-year Treasury yield at 5.127 percent and the Fed funds path repricing toward a March hike. Late-stage AI valuations are the most rate-sensitive private asset class in the world. If the 30-year holds above 5.1 percent into June, the $900 billion mark will face pushback from the LPs that have to write down their portfolios in Q2.

The third risk is the customer concentration story. Anthropic’s revenue base is heavier on a small number of enterprise contracts than the public market typically tolerates. Goldman, JPMorgan, Bain, Brookfield, and TPG are each in the top ten by ARR. That is fine while the contracts grow. It is less fine if any one of those names cuts spend in response to a slowing economy. In a rate-hike scenario with $107 oil, none of those names are guaranteed to expand at the rate the cap table needs.

The Real Signal

Strip out the noise and the signal is simple. The smartest capital in the world has decided that a foundation-model lab with verified enterprise adoption is worth nearly a trillion dollars in private markets, eighteen months before the next big public AI IPO. If the round closes at $900 billion, it is the strongest possible statement that the AI capex cycle has not topped. The compute buildout still has buyers. The enterprise revenue still has runway. The IPO window is still open if anyone wants to use it.

Dario Amodei and Daniela Amodei have built the most defensible AI lab in the world by being the last team to take the meeting and the first team to spend the check on chips. The market has noticed.

What To Watch Next

Three near-term tells. First, whether the round actually closes by month-end, or slips into June. A slip into June would suggest the bond market is doing damage to the term sheet. Second, the size of the strategic allocation to corporate partners. If Microsoft or Salesforce gets in alongside Google, the antitrust risk goes up but so does the commercial backstop. Third, the timing of any commercial milestone disclosure. Anthropic does not need to release a number to justify the valuation, but a clean enterprise ARR disclosure would lock in the comp set ahead of the Q2 fundraising cycle.

Watch the close date. Watch the strategics. Watch the ARR. Everything else is window dressing.