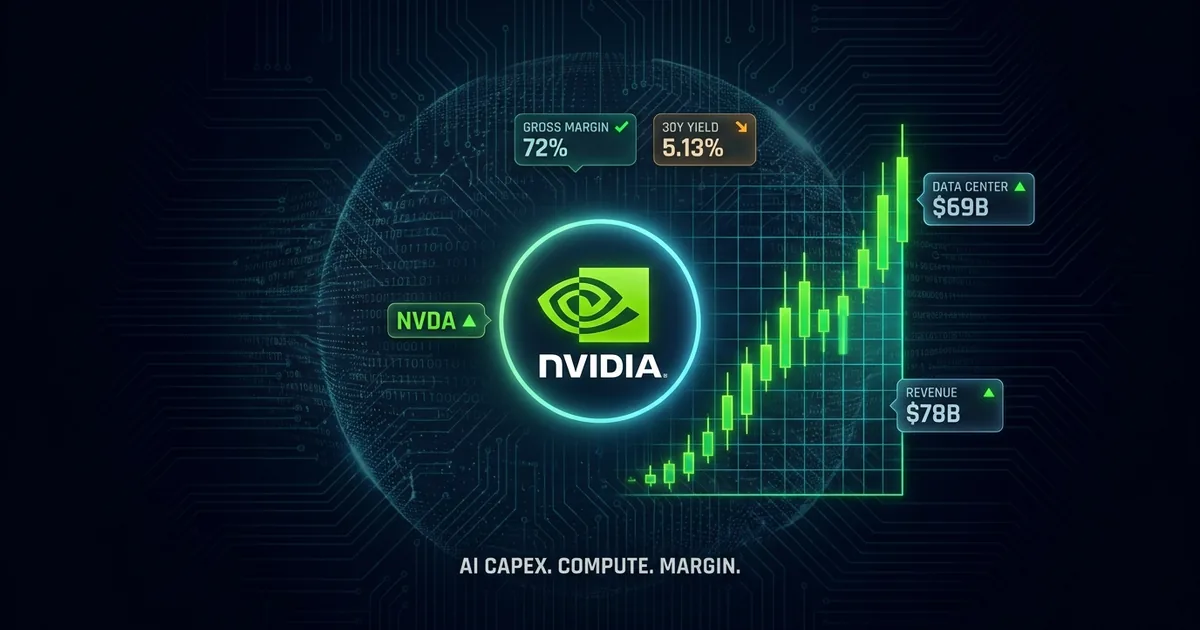

Nvidia drops its first-quarter print after Wednesday’s bell, and the setup could not be more loaded. Wall Street is modeling roughly $78 billion in revenue, $1.77 in adjusted EPS, and a year-over-year top-line expansion in the neighborhood of 77 percent. The buy side wants three things from CEO Jensen Huang: confirmation that Blackwell shipments are running at full capacity, a hard read on China after the Trump-Xi H200 framework, and a number on Vera Rubin orders for the back half of 2026.

What the market is going to get is a referendum on the only trade still levitating this market.

The AI Capex Backstop Is Real Money

The four hyperscalers, Amazon, Alphabet, Meta, and Microsoft, have already committed somewhere between $695 billion and $725 billion of 2026 capex, the bulk of which lands inside Nvidia’s data-center book. Cisco’s $9 billion in AI infrastructure orders for fiscal 2026, disclosed last week, is a downstream tell on how aggressively the rack-level buildout is still running. None of that is going away in 90 days. The question is whether it grows from here, and at what gross margin.

Jensen’s last GTC framing put Blackwell at “sold out for the year” and Vera Rubin in “commercial volume” by the second half. The earnings preview going around the sell side pegs data center revenue as the single number that will move the stock more than the headline beat. Consensus has data center at roughly $69 billion, up from $39.1 billion a year ago.

If that print holds and gross margin stays north of 72 percent, the bull case writes itself. If gross margin slips because the company is pushing Blackwell Ultra into hyperscalers at concessionary pricing to lock in Vera Rubin commitments, the print becomes a sell on the news.

China Is The Hidden Variable

The Trump-Xi summit on May 13 produced a framework allowing Nvidia to sell its H200 chip to roughly 10 named Chinese firms, including Alibaba, Tencent, and ByteDance, under a 75,000-chip license cap. That is real revenue Huang did not have in February. It is also a political risk Huang did not have in February.

Wall Street wants the dollar amount Nvidia is willing to underwrite from the China commercial book. Two analysts on the sell side have put incremental China revenue at $4 billion to $6 billion in the back half. The honest answer from Huang is closer to “we will tell you when the licenses clear,” because the State Department is still finalizing end-user verification under Commerce’s new framework. Anything more aggressive on the call than what Treasury and Commerce have signed off on will draw an immediate pushback from the China hawks on the Senate Banking Committee.

The Cerebras And Apple-Intel Overhang

The competitive picture also changed last week. Cerebras raised more than $5.5 billion in the largest IPO of the year and closed its first session up 68 percent. The company will not threaten Nvidia’s data-center monopoly this quarter, but it puts a public competitor on the board for the first time in two years. Sell-side desks will press Huang on training versus inference workload share, because the Cerebras pitch is built around the inference side.

Apple’s preliminary chip-foundry deal with Intel, brokered with personal Trump involvement and announced May 8, sent Intel into a multi-bagger run that started at $20 and ran past $125. That is not a direct competitive threat to Nvidia in data center, but it is a giant signal that the US chip stack is becoming a multi-foundry, policy-driven market. Nvidia is the biggest beneficiary of an open TSMC, and the second-biggest loser if TSMC capacity gets reallocated to Apple and Intel through political channels.

The Bond Market Headwind

This is the harder problem. The 30-year US Treasury yield closed Friday at 5.127 percent, the highest level since 2007. Fed funds futures now price the next move as a hike by March 2027, not a cut. Long-duration tech is the most rate-sensitive equity in the world, and Nvidia, despite its blowout earnings power, trades on long-duration cash flows.

Goldman’s quantitative desk modeled a 9 percent multiple compression on Nvidia for every 50 basis points the 30-year holds above 5 percent for more than 60 days. The stock can absorb that if the beat is large enough and Huang’s guide is bullish enough. It cannot absorb that if the company prints in line and guides “as expected.” A bond market this hostile turns “in line” into a sell, and the August quad-witch sets up as the next pressure point on the calendar.

What To Watch On The Call

Three real-time tells. First, the gross-margin commentary in the opening remarks. Anything that suggests Blackwell pricing power is intact above 72 percent is bullish. Second, the data-center segment number and the China contribution split. CNBC’s coverage of the Cerebras debut and the broader semiconductor tape last week shows how quickly the buy side is starting to discriminate between training and inference share. If China data center prints north of $1.5 billion in the quarter, the H200 framework is doing more than analysts modeled. Third, the Vera Rubin orderbook commentary. Huang is unlikely to give a hard number, but if he uses the phrase “significantly oversubscribed,” that is the line that moves the stock 5 percent in after-hours.

The Rest Of The Tape

The rest of the week stacks up. Walmart prints Thursday, the closest read on the US consumer under $107 oil. Home Depot reports Tuesday with a profit cut already telegraphed. Target reports Wednesday morning ahead of Nvidia, and the discretionary-versus-staples split could matter for sentiment heading into the chip print. Palo Alto Networks reports Tuesday after the bell, the cybersecurity bellwether of the cycle. Baidu rounds out the China tech read midweek.

Add the FOMC minutes on Wednesday at 2 p.m. and the 20-year Treasury reopening that morning, and there is no single trading day this week without a market-moving print. The macro tape will color how investors read Nvidia’s numbers, not the other way around. That is the inversion that matters for this cycle.

The Trade

The bull case requires Nvidia to print a clean beat on revenue, hold gross margin above 72 percent, give a credible China number, and signal a Vera Rubin orderbook that is meaningfully oversubscribed. Anything less than that into a 5.1 percent 30-year and a $107 oil tape gets sold. The bear case is not that AI demand has cracked. It is that the cost of capital just doubled relative to what the multiple required.

The bond market wrote the script for the week. Nvidia has to deliver the rebuttal. The single chart on the desks Monday morning was not Nvidia’s 50-day moving average. It was the 30-year yield.