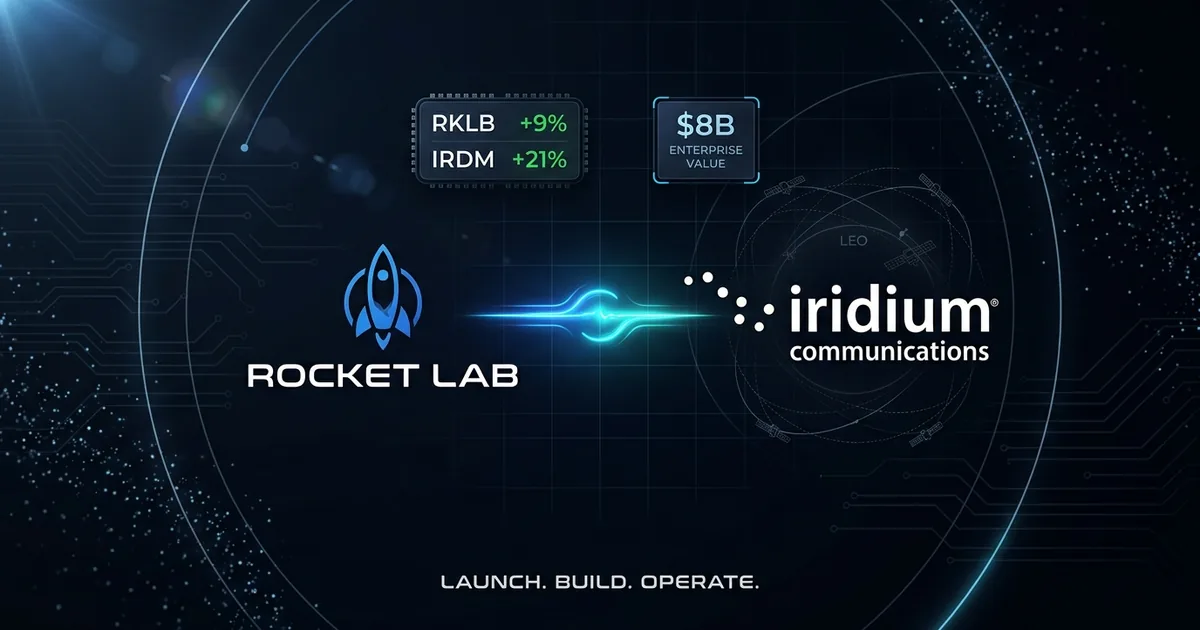

Rocket Lab just made the deal Peter Beck has been building toward for a decade. The New Zealand-born launch company announced a definitive agreement to acquire Iridium Communications for $54 per share in a cash-and-stock transaction valued at approximately $8 billion, and the market is rewarding the ambition: RKLB surged 9% in premarket while IRDM rallied more than 20%.

The deal is the clearest signal yet that the space economy’s center of gravity is shifting from launch-as-a-service to end-to-end vertical integration, and the company that built Electron is betting its future on owning the entire stack from factory floor to orbit.

What the Deal Looks Like on Paper

Iridium stockholders will receive $27.00 in cash plus Rocket Lab shares for each share they hold. The stock component uses an exchange ratio subject to a collar banded between $67.50 and $112.50 per RKLB share, a structure designed to protect both sides from volatility while giving Iridium holders meaningful upside in the combined entity.

Both boards approved the deal unanimously. CNBC reported that the transaction is expected to close by mid-2027, pending Iridium stockholder approval and the usual regulatory clearances. SEC filings from both companies hit EDGAR within the hour, confirming the terms and laying out the integration timeline.

At $8 billion enterprise value, this is one of the largest pure-play space M&A transactions in history, and it transforms Rocket Lab from a launch-and-satellite-manufacturing company into something the industry has never quite seen: a single entity that designs, builds, launches, and operates its own satellite constellations.

The Structural Logic: Escaping the Launch Commodity Trap

Here is the why that matters more than the price tag. The space launch market is commoditizing. SpaceX’s dominance of commercial launch, reinforced by its record-setting Nasdaq debut earlier this month, has compressed margins across the industry. For a company like Rocket Lab, which built its reputation on reliable small-sat launch with Electron and medium-lift ambitions with Neutron, the long-term business model problem was always the same: launch is a razor-thin-margin service business where the customer can always shop for a cheaper ride.

Iridium solves that problem. Its 66-satellite low-Earth-orbit constellation is fully deployed, generating recurring subscription and IoT data revenue from more than 500 partner organizations worldwide. It holds global spectrum rights that took decades and billions to secure. Those are the kinds of assets you cannot build from scratch on any reasonable timeline.

Beck called the combined entity a “space powerhouse,” and for once the label is not hyperbole. Rocket Lab will now design the satellites (Photon bus), manufacture the components (solar panels, reaction wheels, star trackers), launch them on its own rockets, and operate the constellation that generates the revenue. Every link in that chain was previously split across different companies with different incentives and different shareholders. Consolidating them under one roof eliminates the coordination costs and margin leakage that have plagued the space industry for decades.

Why Iridium, Why Now

Iridium was not a random target. The company faces a coming capex cycle as it plans next-generation satellites to eventually succeed the Iridium NEXT constellation. Building those satellites in-house through Rocket Lab’s manufacturing operation, then launching them on Neutron rather than buying rides from competitors, could cut recapitalization costs dramatically. The deal turns a future liability into a structural advantage.

For Rocket Lab, the timing aligns with its broader strategic pivot. The company has spent the last several years acquiring space hardware companies, building out its Photon satellite platform, and positioning Neutron as a reusable medium-lift vehicle. What it lacked was the downstream revenue engine that would make all that vertical integration pay off. Iridium, with its global coverage, government contracts, and established partner ecosystem, is that engine.

Yahoo Finance noted that investors are pricing in the strategic premium. The 20% pop in IRDM shares suggests the market views $54 per share as fair but not extravagant, while the 9% jump in RKLB reflects confidence that the acquisition is accretive rather than a stretch.

What This Means for the Space Industry

The deal reshapes the competitive landscape in ways that extend well beyond the two companies involved. SpaceX already operates this vertically integrated model through Starlink, building and launching its own constellation on its own rockets. But SpaceX has never acquired a legacy satellite operator with existing spectrum and government relationships. Rocket Lab is taking a different path to the same destination: buying what it cannot build fast enough.

For the rest of the launch industry, from United Launch Alliance to Arianespace to Blue Origin, the message is uncomfortable. Launch alone is not a viable standalone business at scale. The value is migrating to the companies that own the satellites, the spectrum, and the customer relationships. Launch is becoming a cost center, not a profit center.

For defense and intelligence customers who rely on Iridium’s constellation for communications, the consolidation raises questions about supply chain concentration. A single company controlling the rocket, the satellite factory, and the constellation is either a resilience advantage or a single point of failure, depending on how the Pentagon views vertical integration in a contested space environment.

The Road to Close

The mid-2027 expected closing gives regulators time to review the deal’s implications for spectrum allocation, defense communications, and market concentration. The collar mechanism on the stock component provides a valuation floor and ceiling that should limit deal risk from market volatility.

The biggest execution risk is integration. Merging a launch company’s engineering culture with a satellite operator’s service culture is the kind of organizational challenge that has tripped up aerospace consolidation plays before. Beck’s track record of operationalizing acquisitions, particularly the rapid integration of SolAero, Sinclair Interplanetary, and Advanced Solutions, suggests he understands the playbook. Whether that playbook scales to an $8 billion deal is the open question.

What is not in question is the direction of the industry. The space economy is consolidating around vertically integrated platforms, and Rocket Lab just placed the biggest bet yet that owning the full stack is the only way to compete with SpaceX’s flywheel. The market, for now, agrees.