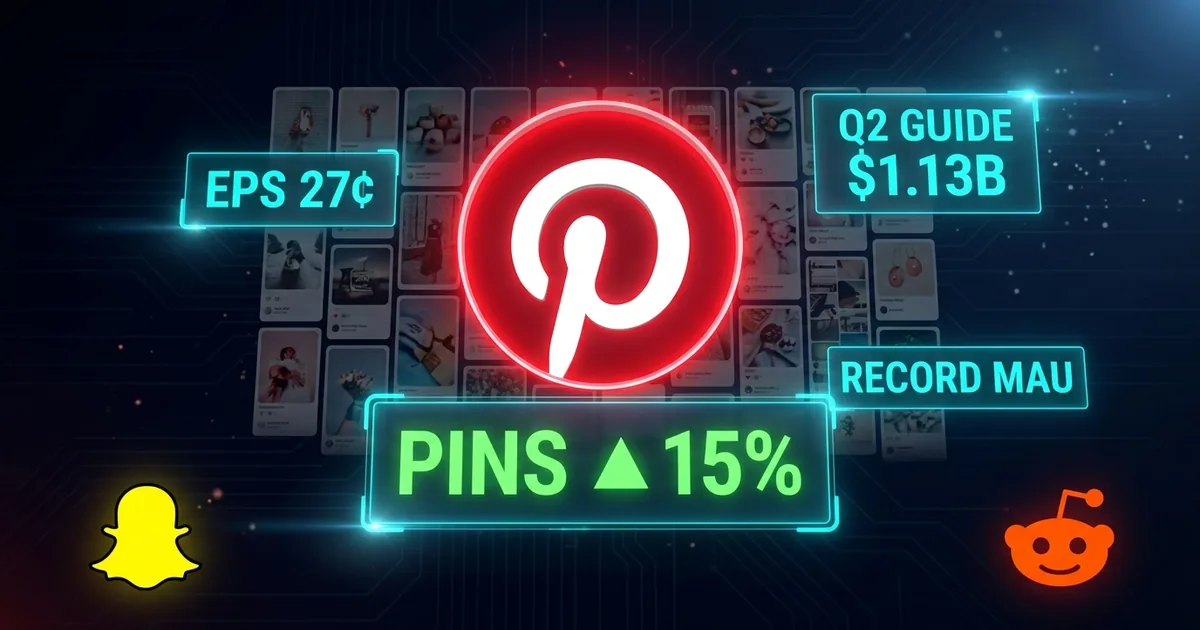

The cleanest Q1 beat of the season did not come from a hyperscaler. It came from a 16-year-old social platform built around mood boards. Pinterest reported adjusted EPS of 27 cents against the 23 cents Wall Street expected, guided Q2 revenue to a $1.133 to $1.153 billion range above the $1.11 billion consensus, and posted record monthly active users on the way. PINS jumped 15 percent on the print. At least seven sell-side desks raised price targets the next morning. In an AI-saturated tape obsessed with Microsoft, Alphabet, and Meta, Pinterest just delivered the kind of operating margin expansion every social platform spent the past year claiming was around the corner.

The wildcard read: the AI-driven ad targeting engine the company rolled out last quarter is doing real work on the income statement, not just on the slide deck. That makes Pinterest the cleanest small-cap test case for whether AI ad-tech is actually moving consumer-platform revenue or just rearranging the cost structure.

The Numbers Wall Street Underestimated

Adjusted EPS of 27 cents is a 17 percent beat against consensus, the largest top-line earnings surprise the company has produced in eight quarters. Q2 revenue guidance landing at $1.133 to $1.153 billion against an $1.11 billion expectation is a 2 to 4 percent overage, which is the kind of guide that resets a sell-side model rather than nudges it. Monthly active users hit a record, and the international cohort that has been the swing variable in the growth story produced positive ARPU growth for the third consecutive quarter.

The combined message is that Pinterest is not just beating estimates. It is structurally outgrowing the model the buy side had been running. That is the kind of print that justifies a 15 percent move and the seven price-target raises that landed Thursday morning.

Why a 15 Percent Beat Matters in This Tape

In a market obsessed with hyperscaler capex, an AI capex bubble argument that gets refreshed every two weeks, and an OpenAI IPO timing question that pulls every other tech equity story along with it, a clean operating beat from a consumer-internet company carries more signal than the same beat would in a normal quarter. Investors looking for AI exposure that is not bottlenecked on Nvidia GPU shipments or hyperscaler power-availability constraints have a small bench to choose from, and Pinterest just printed a result that puts it on that bench.

The relative-value comparison is where the move gets interesting. Meta and Alphabet both delivered solid prints last month, with the AI ad-tech narrative still doing most of the heavy lifting on their multiples. Pinterest now offers the same AI ad-tech narrative at a fraction of the multiple, which is the trade allocators have been hunting for since the Datadog-led Q1 SaaS earnings re-rating already showed AI workloads feeding the software stack rather than eating it. Pinterest is the consumer-internet version of the same trade.

The AI Ad Targeting Engine That Did the Work

The mechanical question every analyst asked Thursday was which line item AI ad targeting is actually moving. The answer Pinterest gave is that the engine is showing up in three places: higher click-through rates on shopper-intent boards, faster conversion on retail-catalog placements, and improved inventory yield on the lower-ARPU international markets. The cumulative effect on the quarter was a measurable lift in effective CPM that translated into the revenue beat without requiring a corresponding lift in active-user growth.

The structural difference with Meta and Alphabet is the data set. Pinterest’s user base is dominated by high-intent shopping queries, with users who treat the platform more like a retail catalog than a social network. AI ad targeting on intent-rich data is a meaningfully easier optimization problem than AI ad targeting on the lower-intent feeds that dominate Meta and Alphabet inventory. Pinterest is not selling a comparable product. It is selling a higher-intent product, and the AI tooling is monetizing the intent more efficiently than the previous-generation algorithmic stack did.

The Sell-Side Re-Rating

Seven sell-side desks raised price targets Thursday morning, including the lift that took the consensus average up by roughly 18 percent on the day. The pattern across the upgrade notes was consistent: analysts moved revenue and operating margin estimates up for the next three quarters and pulled forward margin expansion assumptions that had been deferred to 2027. The stock closed up 15 percent. The forward multiple expanded by closer to 12 percent. The combined effect is a re-rating that puts Pinterest closer to a Snap-and-Reddit cohort than to a legacy social platform.

Per Yahoo Finance’s coverage of the Q1 print and the price-target moves, the most aggressive upgrades came from sell-side desks that had been incrementally bullish on the AI ad-targeting roll-out and now have the quarterly comp they were waiting on. The watch from here is whether the upgrade cohort holds through the next two prints or whether the trade unwinds if Q2 lands inside guidance rather than above.

The Forgotten Social Bench Just Got a Comp

For the broader bench of social and community platforms outside the Meta-Alphabet-Microsoft hyperscaler complex, Pinterest’s print is the comparable transaction the bull cases have been waiting for. Snap, Reddit, Tumblr, Discord, and the smaller community-platform operators all have AI ad-targeting roll-outs in flight, and all of them have been arguing that the margin expansion is around the corner. Pinterest just put a quarterly result on the board that supports the argument with actual numbers.

The differentiation matters. Snap and Reddit have meaningfully different user-intent profiles, and the AI ad-tech read-through is uneven. Pinterest’s high-intent shopping data set is genuinely advantaged. Reddit’s discussion-thread data set is harder to monetize but is where AI training-data licensing has been moving the cost line. Snap’s friend-graph data set sits in the middle. The next cycle of AI ad-tech earnings disclosures will sort which of these benches actually gets re-rated in the same way Pinterest just was.

The Investor Read

For consumer-internet investors, the cleanest takeaway is that Pinterest just produced the best AI-driven beat outside the hyperscaler complex. For sell-side desks, the playbook is to roll the same model template across the rest of the social bench and look for the next comparable result. For the AI capex bubble argument, the print is a quiet rebuttal that the AI investment cycle is actually generating measurable revenue on the operator side, not just on the supplier side.

Per The Motley Fool’s take on the Pinterest print, the longer-term question is whether Pinterest can maintain the operating margin step-up as the AI ad-tech roll-out matures and the easy comp gets harder. The structural answer for Pinterest is yes, because the user-intent data set is the moat, and the moat compounds as the targeting engine gets more training data. The cyclical answer depends on whether retail ad spend holds up through the rest of 2026, which is the variable Pinterest controls less than its own targeting tooling.

Three Reads From Here

First, whether PINS holds the 15 percent move through the next two trading sessions or fades the gain into the lockup of post-earnings selling. Second, whether the next round of social-platform earnings, particularly Snap and Reddit, deliver comparable AI ad-tech read-throughs or surface the limits of the thesis. Third, whether the sell-side upgrade cohort grows or stabilizes inside the seven desks that already moved targets.

The AI capex story has been a hyperscaler story for two years. The Pinterest print is the cleanest signal of the year that the operator side of the equation is starting to deliver, and the social-platform bench just got a comparable result the rest of the cohort will have to either match or explain away.