Micron Technology reports fiscal third-quarter results after the bell on Tuesday, and the stakes have never been higher for the company that has quietly become the backbone of the AI infrastructure buildout. With analysts expecting $19.72 in earnings per share on $34.52 billion in revenue, the print will either validate one of the most explosive stock runs in semiconductor history or expose the first crack in the AI memory thesis.

The Numbers That Matter

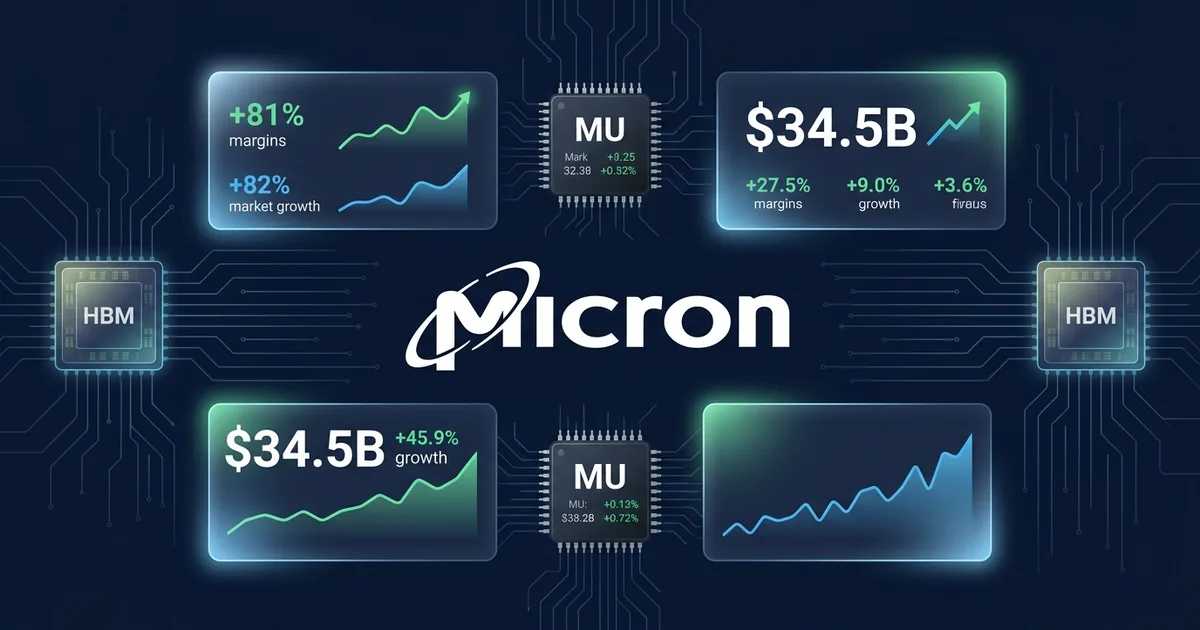

The consensus estimates tell one story: Micron’s own guidance calls for revenue of $33.5 billion (plus or minus $750 million) and non-GAAP EPS of $19.15, with gross margins around 81%. If that margin number holds, it would be the highest in the company’s history and among the best in the entire semiconductor industry. For context, CNBC reported on Monday that the stock dropped more than 13% during the session as part of a broader chip selloff that dragged the Nasdaq down 2.2%.

Against the same quarter a year ago, when Micron posted $1.91 per share on $9.3 billion in revenue, the current consensus implies EPS growth north of 930% and revenue expansion of roughly 271%. Those are not normal numbers. Those are numbers that reflect a company riding a structural demand wave that has reshaped the entire memory industry in 18 months.

The Anthropic Deal and the HBM Flywheel

What separates this earnings cycle from previous ones is the strategic positioning Micron has locked in. The company recently signed a multi-year AI infrastructure agreement with Anthropic, making Micron the primary supplier of HBM, DRAM, and SSDs for Claude’s training and deployment stack. That deal, which includes an equity investment in Anthropic’s latest funding round, signals a shift in how AI companies are securing their supply chains, moving from spot purchases to long-term, vertically integrated partnerships.

The high-bandwidth memory (HBM) business is the engine. Every major AI training cluster, from Nvidia’s GB200 racks to AMD’s MI400 configurations, requires exponentially more memory per chip generation. Micron’s HBM3E production is sold out through 2026, and the company has already certified HBM4 samples with key customers. The question is not whether demand exists. The question is whether Micron can scale production fast enough to capture it without compressing the margins that have turned the stock into a ten-bagger.

Why the Options Market Is Nervous

The options market is pricing a roughly 17% move in either direction off the print. That is enormous implied volatility for a $200 billion-plus company sitting at an all-time high near $1,133. The last time Micron carried this much implied movement into an earnings report, the stock gapped down 8% on a guidance miss that the Street later called a buying opportunity.

The nervousness is not unfounded. Monday’s semiconductor selloff was driven by growing skepticism among institutional investors about whether the hyperscalers’ combined $400 billion-plus in AI capital expenditure this year will generate returns proportional to the spend. Bank of America published a note questioning the near-term monetization timeline, and the DRAM ETF that has become the fastest-growing semiconductor fund of 2026 saw its first significant outflow day. Nvidia fell 4.2%, Broadcom shed 3.1%, Qualcomm dropped 8%, and AMD lost 5.8%.

The Bull Case and the Bear Case

The bull case is straightforward: AI infrastructure spending is a multi-year cycle, not a one-quarter phenomenon. Micron’s HBM capacity is fully allocated, its DRAM pricing power is at a cycle high, and its customer base now includes the most capital-rich companies on the planet. If gross margins hit 81% and the company guides for continued expansion, the stock has room to run toward $1,300.

The bear case centers on a single word: sustainability. If Micron reports 81% gross margins but guides for sequential decline as new HBM capacity comes online from Samsung and SK Hynix, the signal flips. The memory business is historically cyclical, and the last time margins peaked at these levels (never, actually, which is part of the bull argument), the stock was already pricing in perfection. A miss on the guidance, even with a beat on the quarter, could trigger the kind of air pocket that the options market is pricing.

What to Watch After the Close

Three numbers will define the reaction. First, the gross margin: anything below 79% signals pricing pressure. Second, HBM revenue as a share of total DRAM: analysts expect it to cross 30% for the first time. Third, the forward guidance range. If Micron holds $35 billion-plus for Q4 with expanding margins, the AI memory trade has legs. If the guide comes in below consensus with margin compression language, the 17% implied move could go in the wrong direction.

The broader market context matters too. Micron reports into a tape that just sold off hard on AI spending skepticism. A strong print and guide could reverse the narrative overnight and pull the entire semiconductor complex higher. A weak one could accelerate the rotation into defensive names that gained ground on Monday, with Walmart up 2% and Johnson and Johnson reclaiming investor attention.

Either way, after the close on Tuesday, we will know whether the most expensive memory stock in history earned the premium or whether the market finally found the ceiling on the AI infrastructure trade.