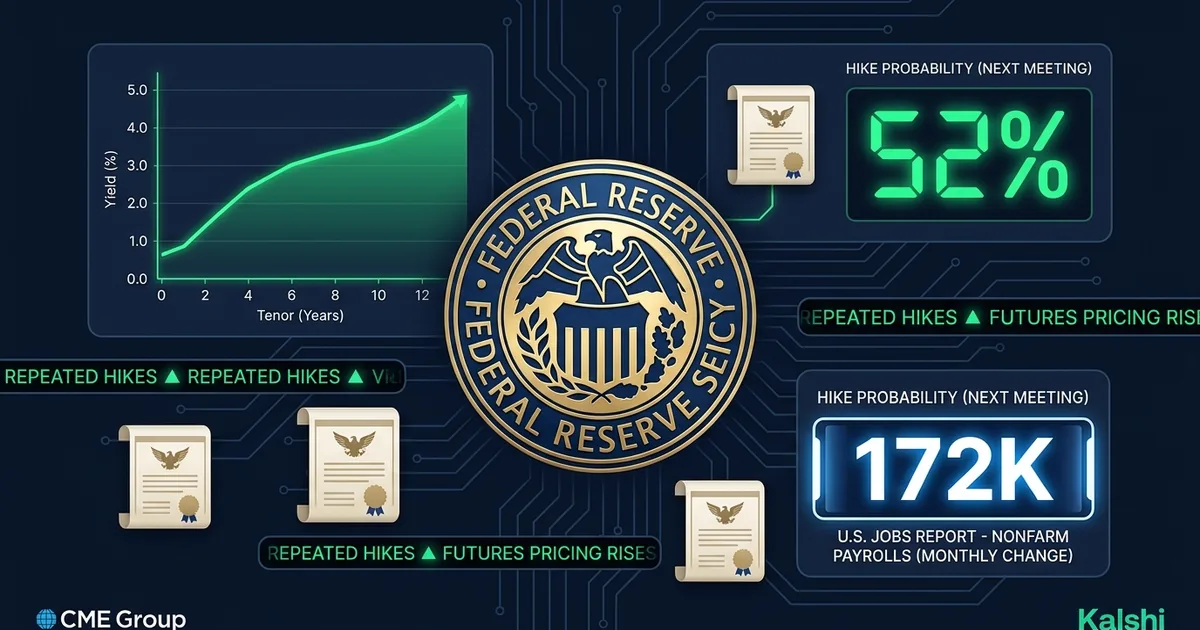

Prediction markets pushed the probability of a Federal Reserve rate increase this year past 52% on Friday, a seismic shift from 25% just one week ago. The catalyst: a May jobs report that blew past expectations and killed whatever remained of the rate-cut narrative.

172,000 Jobs Shattered the Consensus

The Bureau of Labor Statistics reported 172,000 nonfarm payrolls for May, more than double the 80,000 Dow Jones consensus. Average hourly earnings ticked higher. The unemployment rate held steady. By every conventional measure, the labor market is running hotter than the Fed wants it to, and hotter than Wall Street had been pricing.

The reaction was immediate. Treasury yields spiked, with the 10-year climbing sharply on the day. Interest-rate swaps moved to price a quarter-point hike by December, with roughly 60% odds of a move as early as October. The bond market, which had spent months debating how many cuts the Fed might deliver in 2026, pivoted overnight to debating when the first hike lands.

Kalshi prediction market data showed the probability of at least one rate increase before year-end surging from 25.3% to 52% within 48 hours. That is not a gradual repricing. That is a regime change in expectations.

The Inflation Math Has Not Cooperated

The hot jobs number lands on top of an inflation picture that was already uncomfortable. The annual core PCE rate hit 3.8% in the most recent reading, well above the Fed’s 2% target. GDP was revised down to 1.6% annualized in the prior quarter, creating a stagflationary undertone: growth slowing while prices refuse to fall.

BTN covered the GDP and PCE inflation readings last month, and the picture has only tightened since. The Fed is caught between an economy that generates jobs at an aggressive clip and an inflation rate that has stalled well above target. Cutting into that environment was always going to be difficult. The jobs report made it politically and economically impossible.

What Changed on Wall Street

The equity market response was brutal. The Nasdaq Composite dropped 4.18% on Friday, its worst session since the tariff shock of April 2025. The S&P 500 fell 2.64% to 7,383. The Dow shed 695 points. The PHLX Semiconductor Index collapsed over 10%, its worst single day since March 2020, erasing roughly $1.3 trillion in chip-stock market capitalization.

Rate-sensitive sectors bore the heaviest damage. Growth stocks that had rallied on the assumption of easier monetary policy in the back half of 2026 repriced violently. The logic is straightforward: if the Fed is hiking rather than cutting, the discount rate on future earnings goes up, and the stocks most sensitive to that math fall the hardest.

The pain extended to Asia. South Korea’s KOSPI triggered a circuit breaker after plunging over 6%, with Samsung Electronics down 7% and SK Hynix off nearly 10%. Japan’s Nikkei fell 1.3%. The Silicon Review reported that global chip stocks lost $1.7 trillion in combined value over two sessions.

The Fed’s June Meeting Looms

The Federal Open Market Committee meets June 17-18, and markets now expect Chair Jerome Powell to signal that the next move is more likely up than down. No one expects a hike at the June meeting itself, but the forward guidance language matters enormously. If the statement drops any reference to “well-positioned” or “patient,” traders will read it as a green light for a September or October move.

The futures market tells the story in numbers. Fed funds futures for December 2026 have shifted from pricing in one cut to pricing in one hike. That is a swing of roughly 50 basis points in implied expectations over two weeks. For a market that had been positioned for easing, the reversal is punishing.

What This Means for the AI Trade

The rate-hike repricing has immediate implications for the AI infrastructure buildout. Companies like Meta, Alphabet, and Microsoft are committing hundreds of billions to data center construction financed in part through debt markets. Higher rates make that capital more expensive. The cost of the AI arms race just went up.

More broadly, the shift challenges the narrative that underpinned the first half of 2026: strong earnings from the Magnificent Seven plus eventual rate relief equals higher equity prices. If the “eventual rate relief” leg of that thesis is broken, the market needs earnings growth alone to justify current multiples. And at 22 times forward earnings on the S&P 500, the margin for disappointment is thin.

The Fed has not hiked rates since July 2023. If traders are right that a hike is coming before year-end, it would represent the most significant monetary policy reversal since the pivot from tightening to easing in late 2023. The jobs market just told the Fed that its work is not done. The question now is whether the Fed listens.