Dell Technologies reports first-quarter results after Thursday’s close, and the number that matters is not revenue or earnings per share. It is gross margin. Wall Street expects Dell to post adjusted EPS near $3.00 on revenue of roughly $34.95 billion, up about 49% from a year ago, on the strength of a record $43 billion AI server backlog. The question that will actually move the stock is whether selling all those Nvidia-stuffed servers is making Dell any real money.

That tension, enormous top-line growth against a shrinking margin, is the cleanest test yet of whether the AI server business is a great business or just a big one.

The Setup Nvidia Built

Dell walks into this print with the wind at its back. Nvidia reported its own quarter on Wednesday, May 20, posting record revenue of $81.6 billion, up 85% year over year, with data-center sales of $75.2 billion and gross margin around 75%, alongside an $80 billion buyback. That print re-ignited the entire AI infrastructure trade. DELL jumped roughly 15% on Friday, May 22, to a fresh 52-week intraday high near $291, and the stock is up about 92% on the year. Our preview of Nvidia’s quarter laid out the capital-spending backdrop that Dell is now riding.

When the chipmaker prints 75% gross margins and the box-maker prints something closer to 18%, you learn exactly where the value in an AI server actually sits.

The Backlog Is Real

Demand is not the worry. Dell booked $64.1 billion in AI-optimized server orders in fiscal 2026, shipped more than $25 billion of them, and carried a record $43 billion backlog into the new fiscal year, against a stated $50 billion AI server revenue target for fiscal 2027. Those are the numbers, drawn from Dell’s own filings, that have analysts treating the company as the cleanest pure-play on enterprise and sovereign AI buildouts. The order book is the bull case, and it is genuinely strong. To reach the $50 billion target, though, Dell needs enterprise and sovereign-AI demand to keep widening beyond the handful of hyperscalers that drove the first wave, a mix shift that tends to carry better margins than selling racks to cloud giants with their own buying power.

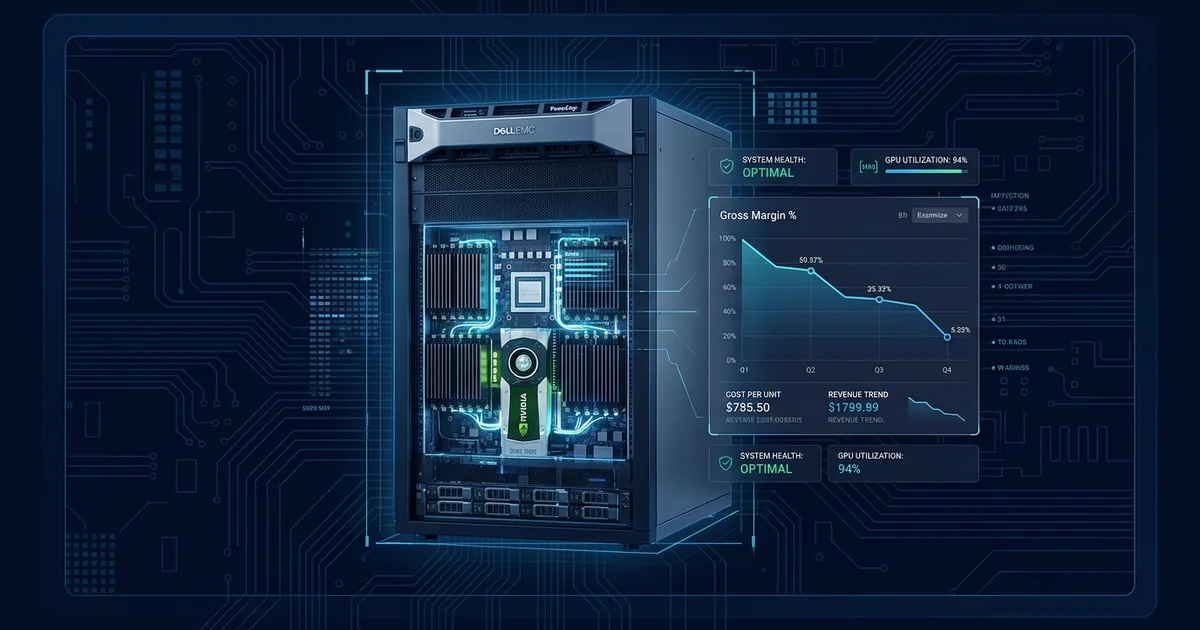

The Margin Problem Hiding Behind the Backlog

Now follow the money. Dell’s company-wide gross margin has compressed from 23.7% in the fourth quarter of fiscal 2025 to 21.1% and then 18.3% across the following two quarters, as Blockonomi laid out in its breakdown of the margin question. The reason is structural: somewhere between 60% and 70% of an AI server’s cost is the Nvidia GPU inside it, which leaves Dell collecting an integrator’s markup on someone else’s silicon. Add rising DRAM and HBM memory prices, and the squeeze tightens unless Dell can pass the cost through.

The metric to watch Thursday is the Infrastructure Solutions Group operating margin, which has swung from 8.8% to 14.8% in recent quarters. A clean step up tells you Dell has pricing power. A slip tells you the AI server land grab is being won on volume at the expense of profit.

What the Analysts Are Doing

The sell side is betting on the volume story. Citigroup lifted its target to $290 from $235, JPMorgan went to $280 from $205 citing easing memory-cost concerns, and Wells Fargo’s Aaron Rakers raised his to $270 from $180, as Barchart noted when DELL hit its new high. The targets are climbing. The margin line is the one number that could make them look early.

The Read-Through to the Whole Trade

Here is our read, framed as analysis rather than reported fact. Dell is the market’s reference price for the merchant AI server. If its margin holds or expands, the bull thesis gets its proof and the rally extends across the box-makers. If it slips, the re-rating will not stop at Dell. The same doubt spreads to Super Micro and HPE, every name selling AI capacity on thin spreads, because if the cleanest operator cannot defend its margin, the market will assume none of them can. That is the real reason Thursday matters beyond Dell’s own shareholders: it is a referendum on whether the integrator layer of the AI buildout can earn a durable profit, or is destined to be the thin-margin middleman between Nvidia and the enterprise.

The Bottom Line on Thursday

Revenue will be big. It is supposed to be. The print that decides the next leg is the gross-margin line and the ISG operating margin underneath it. Hold the line, and the “AI revenue at any margin” story keeps working. Lose it, and Thursday becomes the first real crack in the AI infrastructure trade since Nvidia reminded everyone how good the top of the stack still has it.