President Lee Jae Myung just bet the country’s industrial future on a single thesis: whoever controls the memory chip supply chain controls the AI era.

A National Moonshot Built on Two Companies

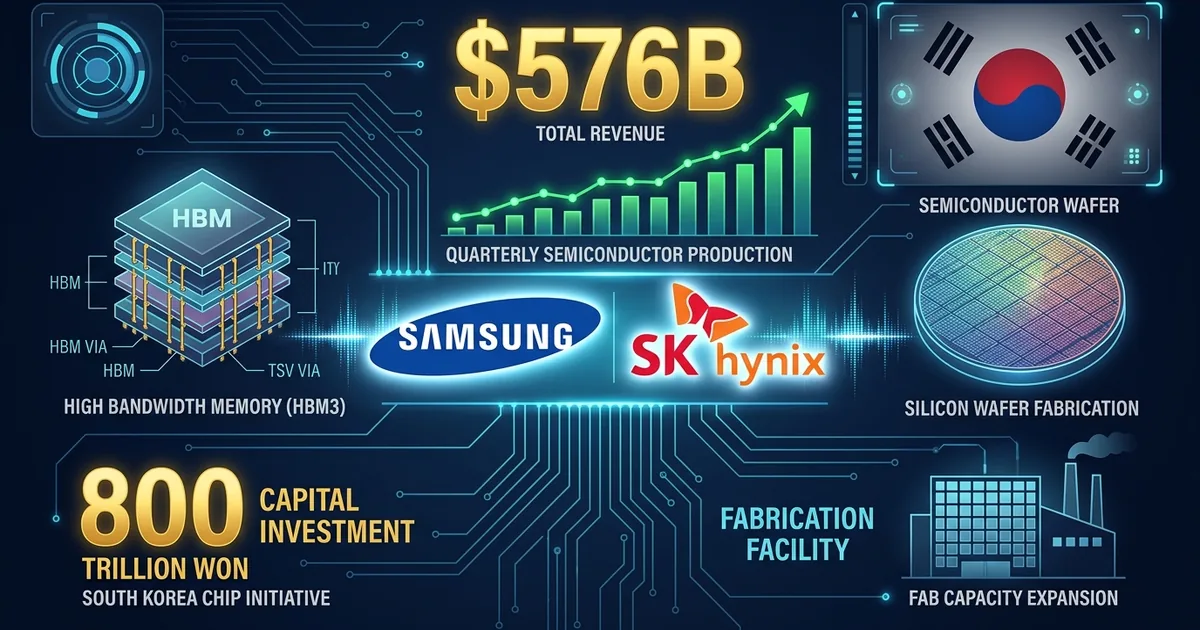

South Korea on June 29 unveiled the largest semiconductor investment plan any single country has ever announced, a sweeping $576 billion initiative anchored by Samsung Electronics and SK Hynix. The two chip giants will each build two new fabrication plants in the southwestern city of Gwangju, forming the backbone of what President Lee described as a national “great leap forward” centered on semiconductors, physical AI, and data centers.

The total package, denominated at 800 trillion won, flows across multiple channels: new fabs, expanded production of high-bandwidth memory chips, AI data center construction, and robotics initiatives. Samsung Chairman Lee Jae-yong confirmed his company’s commitment at the announcement, positioning the investment as a direct response to the global AI compute shortage that has turned memory chips into the most strategically important components in the technology supply chain.

Why Memory Chips Are the Bottleneck

The money follows the physics. Every AI model that runs inference at scale needs high-bandwidth memory to feed data to GPUs fast enough to keep them busy. SK Hynix is the dominant supplier of advanced HBM chips to Nvidia, and its order book is effectively sold out through 2027. Samsung has been investing heavily to close the technology gap, but its HBM3E yields have lagged behind its domestic rival, costing it share in the most lucrative segment of the memory market.

South Korea’s bet is that the HBM supply deficit will persist for years, not months. Alphabet’s 2026 capex guidance alone sits at $180 billion to $190 billion, and Google has already restricted partners’ access to compute capacity because demand exceeds supply. Meta, Microsoft, Amazon, and a dozen sovereign AI programs are all competing for the same chip allocation. The country that can manufacture the most advanced memory at scale sets the price for the entire AI stack.

The Regional Power Play

The initiative is not just an industrial policy play. It is a geopolitical one. South Korea’s southwestern Gwangju province and South Jeolla region will invest an additional 5 to 20 trillion won in supporting infrastructure, while a separate 81 trillion won package funds a chip packaging cluster in the Chungcheong area near Seoul.

This geographic dispersion is deliberate. South Korea’s semiconductor industry has historically concentrated around Icheon and Pyeongtaek in the north, dangerously close to the North Korean border. Spreading production south diversifies risk and creates new regional economic centers, a pattern the US has followed with the CHIPS Act’s Arizona and Ohio fab investments.

The timing also responds to competitive pressure from every direction. The US is subsidizing Intel, TSMC, and Samsung fabs on American soil. Japan is rebuilding its chip industry with Rapidus. China continues to pour money into domestic alternatives despite export controls. SK Hynix’s recently announced $29 billion Nasdaq listing gives it access to American capital markets, but the production capacity still needs to exist in Korea to serve the customers lining up.

What the Numbers Actually Buy

At $576 billion, the initiative dwarfs the US CHIPS Act’s $52 billion authorization and Europe’s roughly $47 billion European Chips Act. But direct comparison misses the point. Most of South Korea’s figure represents private-sector capital expenditure by Samsung and SK Hynix that would have happened regardless, now coordinated under a government framework that adds tax incentives, infrastructure commitments, and regulatory fast-tracking.

The real policy innovation is the government’s role as coordinator rather than funder. By aligning Samsung and SK Hynix’s investment timelines, sharing infrastructure costs, and providing planning certainty, Seoul is reducing the risk that either company under-invests relative to demand. In a market where a single quarter of delayed capacity can mean billions in lost revenue, that coordination function may be worth more than the subsidy dollars themselves.

The Bet Within the Bet

President Lee called semiconductors, physical AI, and data centers a “triple axis.” The phrasing reveals the strategic logic: South Korea is not just betting on chips. It is betting that vertical integration, from memory fabrication to AI training infrastructure to edge deployment, will be more valuable than any single layer of the stack. If that thesis holds, the $576 billion is an investment in capturing the entire value chain. If it does not, the country will have built the world’s most expensive commodity manufacturing base.

The answer depends on whether AI’s current trajectory, capital-intensive, compute-hungry, scaling relentlessly, continues or hits a wall. Every major tech company’s spending plans suggest the trajectory holds. South Korea is betting its industrial policy on the same assumption.