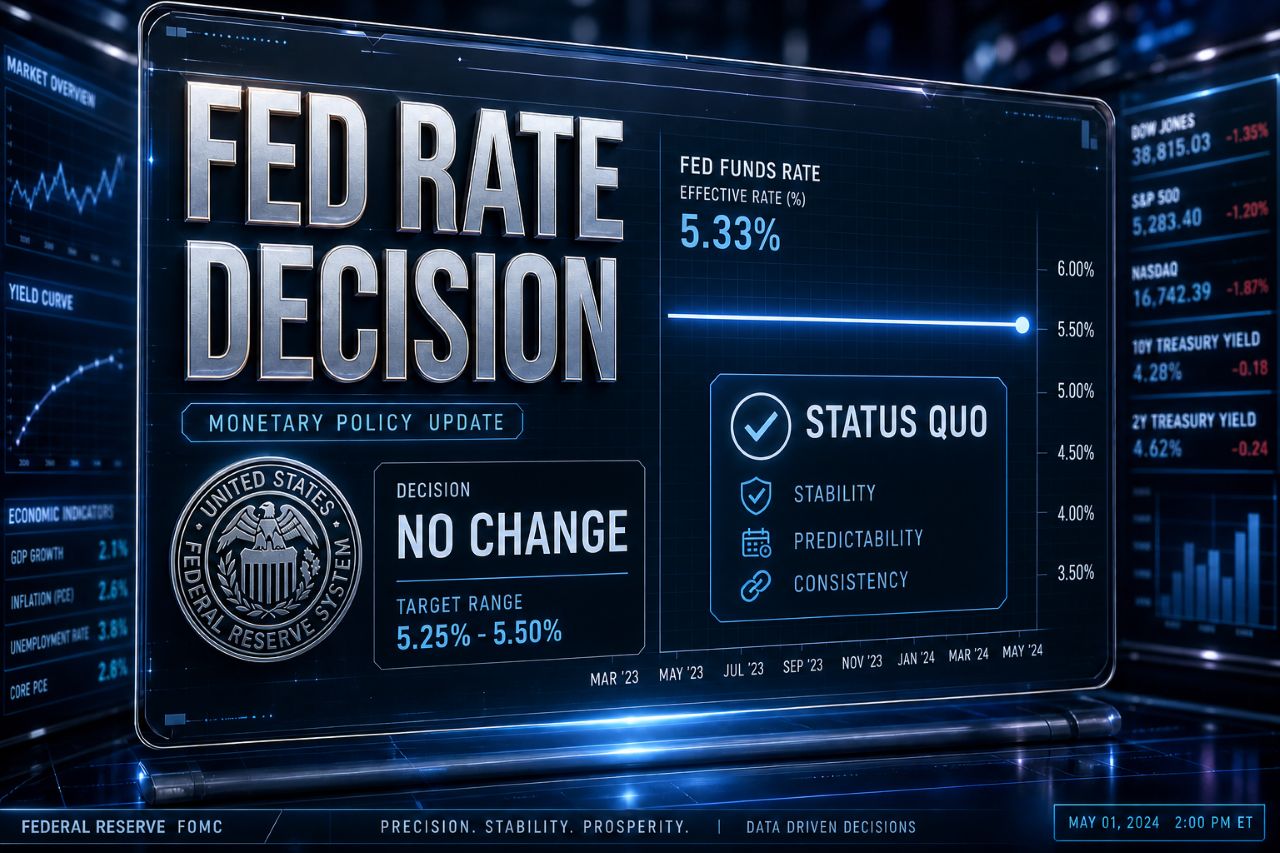

For sixteen years, Jerome Powell has been the most powerful man in monetary policy. At 2 p.m. Eastern this afternoon, he holds his last gavel. The Federal Open Market Committee is widely expected to keep rates pinned at 3.5% to 3.75% for the third meeting in a row, an outcome priced at essentially 100% probability across every major rate-futures market. The headline event will not be the rate decision. It will be the man delivering it, walking out of the Eccles Building for the last time as chair while his almost-certain successor, Kevin Warsh, sits a few miles down the street awaiting confirmation.

On paper, today is a non-event. In practice, it is the most consequential transition in central banking since Ben Bernanke handed Powell the keys in 2014.

Why The Fed Is Holding

Inflation is running at its highest level in nearly two years. Headline CPI is being pushed up by oil, with U.S. crude back near $100 a barrel and pump prices at $4.18 a gallon, the highest since the 2022 spike. Core inflation has reaccelerated as well, partly because supply chains are still digesting the spillover effects of the Iran war and partly because services prices remain stubbornly sticky. Cutting rates in this environment would be a political nightmare for any chair, particularly one trying to walk out the door cleanly.

At the same time, the labor market is softening. Unemployment ticked up in March and again in April. Wage growth is slowing. The Fed sits at the awkward midpoint of its dual mandate, with inflation pressure on one side and employment pressure on the other. A pause is the only honest answer.

Powell’s Legacy

Powell will be remembered for three big calls. The 2020 rate cuts and emergency facilities that prevented a depression-style collapse during the pandemic. The 2022 rate hikes, the most aggressive in four decades, that broke the back of post-pandemic inflation without tipping the economy into recession. And the much harder, much less photogenic year of 2025, when he held rates roughly steady through political pressure that included an open Treasury Department probe into his personal conduct.

That probe, run by U.S. Attorney Jeanine Pirro, was quietly closed last Friday. The timing was no accident. With the investigation off the table, Senator Thom Tillis announced over the weekend that he was prepared to advance Warsh’s nomination, and the Senate Banking Committee has now scheduled the confirmation vote for 10 a.m. today, four hours before Powell’s final meeting concludes. The optics are deliberate. Washington is sending the markets a coordinated signal: orderly transition, no political mess, no reason to panic.

The Warsh Question

Kevin Warsh is not a typical Fed chair pick. He is a former Morgan Stanley investment banker and a Bush-era Fed governor who has spent the last decade as a fellow at the Hoover Institution and a regular speaker on the policy circuit. He is widely seen as more hawkish than Powell, more skeptical of large-scale asset purchases, and more inclined to let markets discover their own clearing prices rather than smoothing volatility with forward guidance.

That is not nothing for a Treasury market that has been shaken by Jamie Dimon and Ray Dalio over the past 48 hours. Both billionaires have warned in unusually direct language about a potential bond market crisis triggered by U.S. debt levels. Dimon’s exact phrase yesterday was, “The way it’s going now, there will be some kind of bond crisis, and then we’ll have to deal with it.” That is the macro backdrop into which Warsh would step.

A more hawkish Fed, in theory, is good for bond holders because it disciplines inflation. But a more hawkish Fed that gets the timing wrong as the economy slows is poison for risk assets. Stocks have rallied through the Iran war, through the OpenAI revenue scare, and through the Strait of Hormuz crisis. They are priced for a soft landing. Warsh’s first move in office will set the tone for whether that landing is achievable.

What To Listen For This Afternoon

The press conference matters more than the statement. Powell will face questions about three things: the timing of the next rate cut, his personal view of Warsh’s nomination, and the inflation outlook now that the UAE has just exited OPEC. Expect him to dodge the second one with grace and to lean cautious on the third.

The single most important sentence will be how Powell describes the balance of risks. If he says inflation risks have moderated, the bond market rallies and the dollar weakens. If he says inflation risks remain elevated, the curve flattens further and stocks could give back gains.

Watch the dot plot, too. If the median 2026 dot moves up rather than down, that is a hawkish handoff to Warsh, who will inherit a committee already inclined toward holding rates higher for longer.

What This Means For Investors And Consumers

This is not a meeting where you want to be tactical. The Fed will not cut. The Fed will not raise. The signal will come in the language. For now, the playbook for the next 30 days looks like this: short-duration Treasuries continue to be the safest carry trade in the market, the dollar holds firm against most majors except the yen, and equity volatility stays bid until the Mag 7 earnings clear after the bell.

For consumers, the implications are direct. Mortgage rates, currently averaging around 7.4% on a 30-year, are not going to fall meaningfully until the Fed actually cuts. Auto loans, credit cards, home-equity lines, all stay punishing. The economy has to absorb that for at least another six months, possibly longer if Warsh proves as hawkish as his record suggests. Detailed coverage of the FOMC mechanics and the rate decision is available at CNBC, where the press conference will be live-blogged in detail.

The Last Word

Powell walks out today with one of the harder records in modern central banking. He inherited zero rates, navigated a pandemic, broke the back of inflation, and survived a political environment that would have broken most of his predecessors. Whether Warsh has the temperament to do the same job in a more polarized country and a more fractured global economy is the open question of 2026.

The committee Warsh inherits will be tested almost immediately. Oil shocks, fiscal stress, a labor market in transition, and an AI capex cycle that is starting to wobble. Each one alone is a chair-defining moment. Together they are the most challenging macro setup since 2008.

By 2 p.m. tomorrow, we will have one less question to ask. By the end of the year, we will know whether the Fed’s hawkish handoff was the right call or the kind of policy mistake that takes a decade to undo.