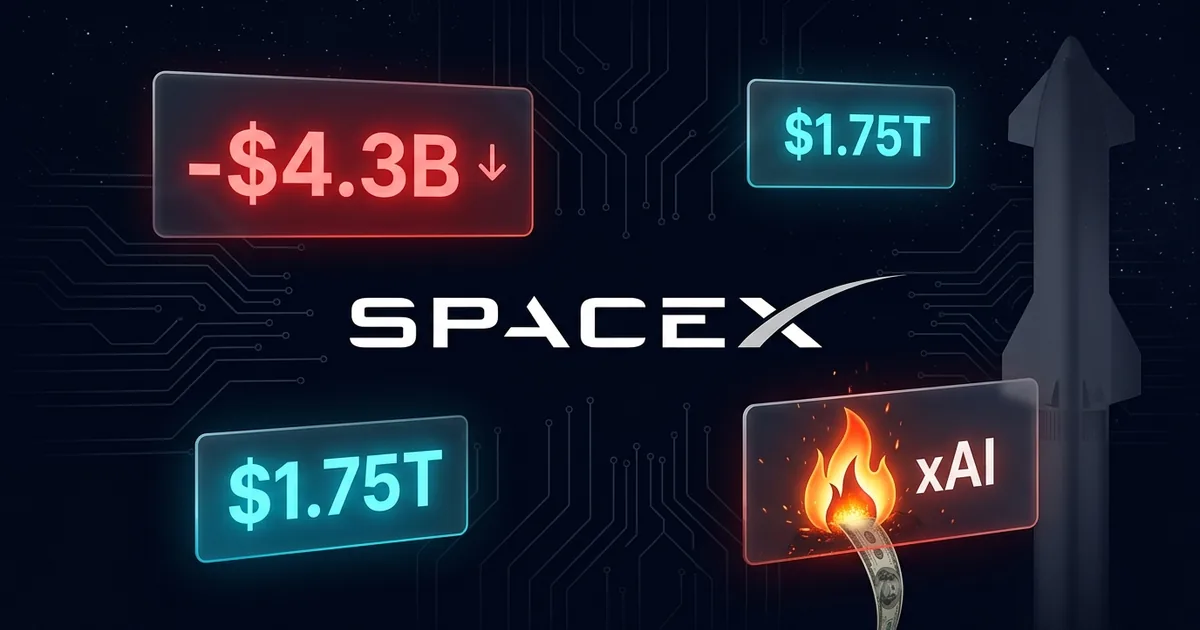

SpaceX filed its S-1 with the Securities and Exchange Commission on May 20, 2026, setting up what would be the largest initial public offering in history at a valuation near $1.75 trillion. Then everyone read past the headline number to the line where the company lost $4.3 billion in a single quarter, and the obvious question landed: what exactly is on fire here?

The Number That Stops You: A $4.3 Billion Quarterly Loss

SpaceX is asking public markets for up to $75 billion, a raise that would dwarf Saudi Aramco’s 2020 debut and rewrite the record books, as Fortune reported when the prospectus dropped. The company booked $18.6 billion in revenue for 2025, up 33% from the year before, which is the kind of growth that justifies a trillion-dollar story. The trouble sits one line down. For the three months ended March 31, 2026, SpaceX reported a net loss of roughly $4.3 billion against revenue of about $4.6 billion. A company losing nearly a dollar for every dollar it takes in is not, on its face, a company you price at $1.75 trillion.

Follow the Capex, and the Story Changes

Here is where the deal-room read diverges from the headline. The loss is not coming from rockets. The S-1’s segment disclosures, which TechCrunch broke down after the filing, show where the cash actually went in the first quarter: about $7.7 billion poured into AI infrastructure, against roughly $1 billion for the space business and $1.3 billion for Starlink. That AI line did not exist in this form a year ago. It arrived in February 2026, when SpaceX folded Elon Musk’s xAI into the company in the merger that built the trillion-dollar IPO.

So the money furnace has a name, and it is not Starship. It is the GPU bill. xAI is in the most capital-intensive phase any AI company faces, buying compute by the gigawatt, and consolidating it into SpaceX means its losses now flow straight onto the same income statement investors are being asked to value at $1.75 trillion.

The Rocket Business Is Actually Fine

Strip xAI out and the picture inverts. The launch segment posted an operating loss of around $657 million for 2025, but that figure is almost entirely Starship research and development, roughly $3 billion in 2025 alone, with the filing acknowledging more than $15 billion committed to the program beyond original estimates. That is not a broken business. That is the dominant force in commercial launch choosing to plow its margins into the next vehicle, which the company expects to begin delivering payloads to orbit in the second half of 2026.

Starlink, the other half of the core, looks even stronger. The filing reports 10.3 million subscribers across 164 countries and roughly 9,600 satellites in orbit as of the end of March. That is a subscription business with global reach and a widening moat, the kind of recurring revenue Wall Street pays premiums for. The cash-generative core is real. It is just being asked to carry a passenger.

Three Companies, One Price Tag

The honest way to describe what SpaceX is selling is three businesses with three completely different financial profiles, bundled under a single number. There is a profitable launch operation that dominates the commercial market. There is a fast-scaling connectivity business in Starlink. And there is xAI, a pre-profit AI lab burning capital at a rate that turns the consolidated statements red. Pricing all three as one $1.75 trillion entity asks investors to accept the AI bet at the rocket company’s valuation, and to trust that Musk’s cross-subsidy logic, launch and Starlink cash funding the GPU war, holds up under public-market scrutiny it has never faced.

That bundling is a feature for Musk and a question for everyone else. It lets the strongest assets carry the riskiest one, and it makes the loss line look scarier than the underlying space business deserves. It also means a public SpaceX shareholder is, like it or not, making a high-stakes bet on xAI winning a compute race against OpenAI, Google, and Anthropic, the last of which just leased Musk’s own Colossus supercomputer in a deal that said as much about xAI’s cash needs as Anthropic’s compute hunger.

The Story Sells the Multiple, the Spreadsheet Tests It

SpaceX is not shy about the narrative. The prospectus frames a total addressable market of $28.5 trillion and a mission to make life multiplanetary, language that belongs in a manifesto more than a risk-factors section. That story is doing real work, because it is what justifies paying $1.75 trillion for a company currently posting nine-figure quarterly losses. Strip the mission rhetoric and you are underwriting a launch business, a satellite internet provider, and a cash-hungry AI lab, priced for a future none of them has reached yet.

The governance fine print deserves the same scrutiny. Anyone buying into a Musk-controlled company buys in knowing the founder keeps the steering wheel, sets the cross-subsidy logic, and can move capital between the rocket business and the GPU business as he sees fit. That has produced extraordinary outcomes at SpaceX before. It also means the people funding xAI’s compute war through their shares will have limited say in how fast that furnace burns.

What to Watch Before June

The filing points to a Nasdaq listing under the ticker SPCX as early as June 2026. Between now and then, the number that matters is not the $1.75 trillion. It is whether the roadshow can convince institutions to underwrite xAI’s burn at a space company’s multiple. If they segment it in their heads the way the S-1 segments it on paper, the launch and Starlink story sells itself. If they price the whole thing on that $4.3 billion loss, the largest IPO in history could open to a market that has already decided which part of SpaceX is the furnace.