Samsung Electronics just fired the starting gun on the next phase of the AI memory wars, and for the first time in over a year, it is the one setting the pace.

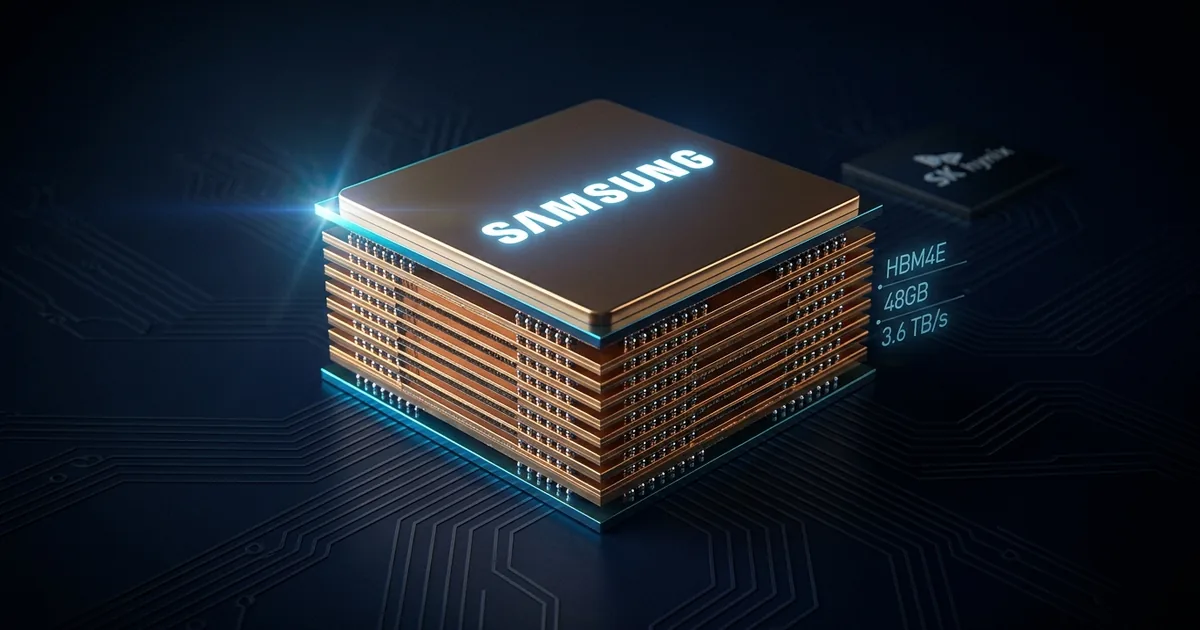

The South Korean chipmaker announced on May 29 that it has begun shipping 12-layer HBM4E high-bandwidth memory chip samples to customers globally, marking the world’s first shipment of the next-generation AI memory product. Samsung shares rallied as much as 6.5% on the news, a reaction that speaks to just how much the market cares about who leads in this particular race.

Why HBM4E Is the Chip That Matters Most Right Now

High-bandwidth memory is the bottleneck component in every AI accelerator worth talking about. Nvidia’s next-generation GPUs, AMD’s MI-series chips, and the custom silicon flooding out of Amazon, Google, and Microsoft all depend on stacking these memory dies as close to the processor as physically possible. The faster and denser the memory, the faster the model trains.

Samsung’s HBM4E pushes that frontier further. The 12-layer stack delivers speeds of up to 16 gigabits per second with a memory bandwidth of 3.6 terabytes per second, representing a 20% leap over HBM4 chips. Capacity hits 48 gigabytes per stack, a 30% jump from the prior generation. Samsung is also developing an 8-layer 32GB variant and a 16-layer 64GB version, signaling this is not a one-shot demo but a full product roadmap.

Energy efficiency improved by 16%, and thermal resistance dropped by more than 14% compared to HBM4, according to Samsung’s technical disclosure. In AI data centers where power and cooling are the binding constraints on how many GPUs you can rack, those numbers translate directly into more compute per watt.

Samsung Needed This Win

The context here matters as much as the specs. SK Hynix has dominated the HBM market with roughly 57% share as of late 2025, compared to Samsung’s 22%. That gap opened because SK Hynix was first to ship HBM3E at volume and locked in supply agreements with Nvidia before Samsung could match quality yields.

Samsung has been playing catch-up for over a year. The company accelerated its HBM4E timeline and delivered samples just three months after beginning mass production of HBM4, a pace that suggests the manufacturing challenges that plagued its earlier HBM3E ramp may be behind it. SK Hynix is not expected to deliver HBM4E samples until the second half of 2026, giving Samsung a meaningful head start.

Whether that head start converts into lasting market share depends on yield rates at scale and whether Nvidia and other GPU makers qualify Samsung’s chips for their flagship products. Qualification is where Samsung stumbled before, and the memory business has learned the hard way that first-to-sample does not always mean first-to-volume.

The AI Memory Market Is About to Get Much Bigger

The stakes are enormous. The AI accelerator market is projected to exceed $200 billion annually by 2028, and HBM accounts for a growing slice of the bill of materials in every high-end chip. Micron, the third major HBM player, recently crossed the $1 trillion market cap on the strength of its own AI memory ramp, underscoring how central this component has become to semiconductor valuations.

Samsung’s move also lands in a week where the broader AI supply chain story dominated markets. Dell Technologies saw its stock surge over 30% after reporting AI server revenue of $16.1 billion, and Snowflake rallied 38% after announcing a $6 billion AWS partnership. The common thread across all these moves is the same: companies positioned in the physical infrastructure layer of AI are being repriced aggressively upward.

The Pricing Power Question

There is a financial dimension to Samsung’s timing that the semiconductor analysts will zero in on quickly. HBM commands dramatically higher margins than commodity DRAM. SK Hynix has been able to charge premium prices precisely because it had the market nearly to itself at the leading edge. If Samsung can credibly offer a competitive HBM4E product at volume, it puts downward pressure on SK Hynix’s pricing power and gives the hyperscalers a second qualified supplier to negotiate against.

For Samsung’s semiconductor division, which has been underperforming relative to its memory peers, a successful HBM4E ramp could be transformative. The unit has been hemorrhaging market share and margin in the commodity DRAM and NAND segments for quarters. HBM is the escape hatch: a high-margin, supply-constrained product where demand is growing faster than any single manufacturer can serve.

What Comes Next

Samsung’s 6.5% stock pop on sample shipments tells you the market is hungry for evidence that the company can compete at the top of the HBM stack again. The real test comes in the second half of 2026, when volume production ramps and Nvidia’s next-generation Blackwell Ultra and Rubin platforms go into mass production. Both will require HBM4E at scale.

If Samsung can convert its first-mover advantage on samples into qualified, high-yield volume production before SK Hynix catches up, the AI memory market could shift from a one-horse race to a genuine two-way contest. For the hyperscalers spending tens of billions on AI infrastructure each quarter, that competition cannot come soon enough.