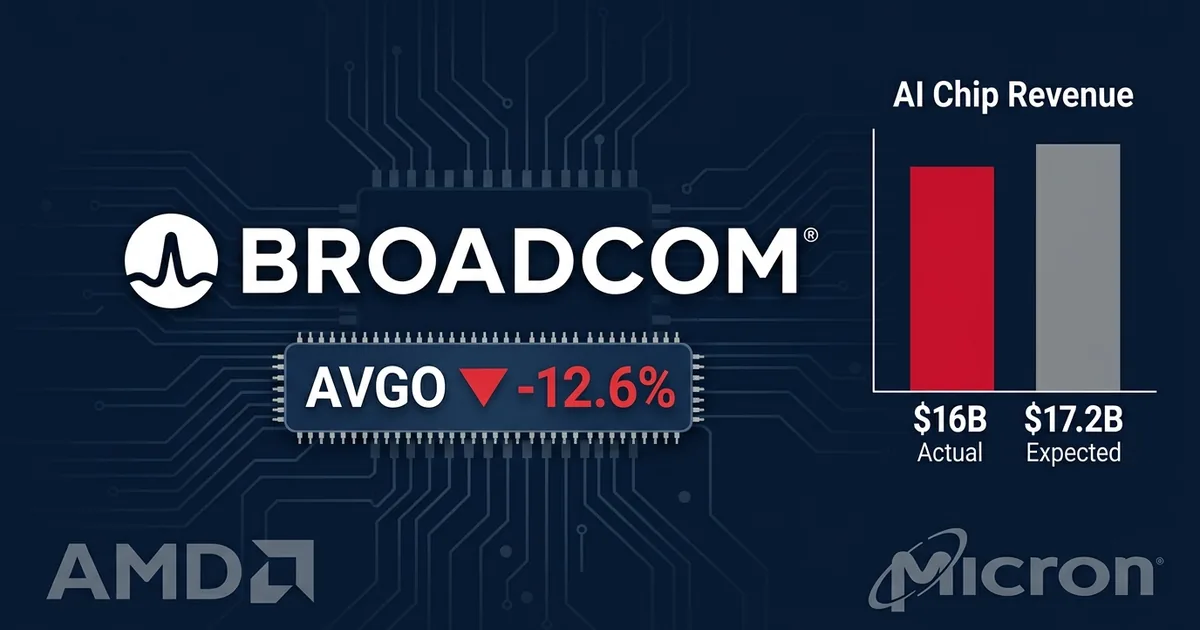

Broadcom just delivered the number that broke the AI trade’s winning streak. The chipmaker’s fiscal Q3 guidance landed at $16 billion in AI semiconductor revenue, a full $1.2 billion below the $17.2 billion Wall Street had penciled in, and the stock cratered 12.6% in a single session, its worst day since January 2025.

The Miss That Moved Everything

CEO Hock Tan held the company’s full-year AI chip forecast at $56 billion, declining to raise the target even as custom silicon adoption has accelerated across hyperscaler clients. Analysts had expected $57.6 billion. Bloomberg reported Wednesday that investors were bracing for a blowout quarter, not a hold-the-line moment, and the gap between expectation and reality wiped roughly $80 billion off Broadcom’s market cap in hours.

The critical detail: Broadcom is not shrinking. Its AI chip business is still enormous, still growing, still the backbone of custom ASIC programs for Google, Meta, and ByteDance. But the market had priced in acceleration, not steady state. When Tan signaled that the ramp would follow the original trajectory rather than steepen, the trade turned.

Where the Money Went

What happened next was the sharpest single-session sector rotation of 2026. Investors did not simply sell Broadcom. They sold the entire AI semiconductor complex and rotated capital into sectors that had been left behind during the chip boom.

The Dow Jones Industrial Average rallied 874.86 points to close at a record 51,561.93, a 1.73% gain driven by healthcare, financials, and industrials. UnitedHealth Group surged 5.36%. Goldman Sachs climbed 4.98%. Merck added 4.86%. Johnson & Johnson rose 4.6%. JPMorgan Chase gained 3.3%.

The Nasdaq Composite, by contrast, slipped 0.09%. The S&P 500 managed a 0.4% gain only because the rotation into non-tech heavyweights offset the chip selloff. AMD fell 3.6%. Micron dropped 7.7%. The Philadelphia Semiconductor Index (SOXX) declined 2.1%.

This is not a market that lost confidence in AI. This is a market that decided the AI infrastructure buildout, while real, will not deliver infinite sequential upside every quarter, and repositioned accordingly.

The Capex Cycle Question

Broadcom’s guidance miss lands at an inflection point for the entire AI capex cycle. CNBC reported Thursday that the rotation out of chip names into non-tech stocks was the most pronounced since the January 2025 DeepSeek selloff, when a Chinese AI startup’s cost claims briefly shook confidence in the entire Western AI infrastructure thesis.

The parallel is instructive. In January 2025, the concern was that AI compute might get cheaper fast enough to undercut chipmaker margins. This time, the concern is different: not that AI spending is collapsing, but that the rate of growth may be normalizing. Alphabet just raised $85 billion for AI infrastructure. Microsoft is building out its MAI model family on Azure. The hyperscalers are still spending. But the market is starting to price the difference between “spending a lot” and “spending more than last quarter’s a lot.”

The broader semiconductor index tells the story clearly. The SOXX dropped 2.1% on the session, with nearly every major chip name caught in the downdraft. AMD, which competes directly with Broadcom in the custom AI accelerator market, fell 3.6% despite having no company-specific news. Micron Technology, which supplies memory chips for AI training rigs, dropped 7.7%. Even Nvidia, the undisputed leader in GPU-based AI compute, saw selling pressure as investors recalibrated expectations across the entire supply chain.

Broadcom’s earlier earnings report, which BTN covered when the company hit its $10.7 billion quarterly target, showed a company executing well on existing demand. The forward guidance miss is about the slope of the curve, not the direction.

What Comes Next

The rotation has implications beyond one earnings print. Healthcare and financial stocks have been relative underperformers for most of 2026 as AI mania consumed incremental capital. Thursday’s move suggests that at least some institutional money is now looking for value outside the semiconductor complex, particularly in sectors with strong cash flows and less narrative risk.

For AI chip investors, the question is whether Broadcom’s conservative guidance reflects genuine demand moderation or simply Tan’s well-known preference for under-promising. The company’s fiscal year ends in October. If Q3 actuals land above the $16 billion guide, the stock likely recovers. If they land at or below, the rotation accelerates.

The timing matters. Broadcom’s next earnings print arrives just weeks before Nvidia’s, and both companies serve as bellwethers for the AI infrastructure cycle. A soft read from Broadcom followed by a strong Nvidia quarter would confirm that this is a company-specific issue. A soft read from both would validate the sector rotation as a structural repricing, not a one-day reaction.

The AI infrastructure story is not over. But the market just signaled that it will no longer pay peak multiples for companies delivering growth that merely meets the prior forecast. In the next phase of the AI buildout, execution alone will not be enough. Investors want acceleration, and Broadcom just told them to wait.