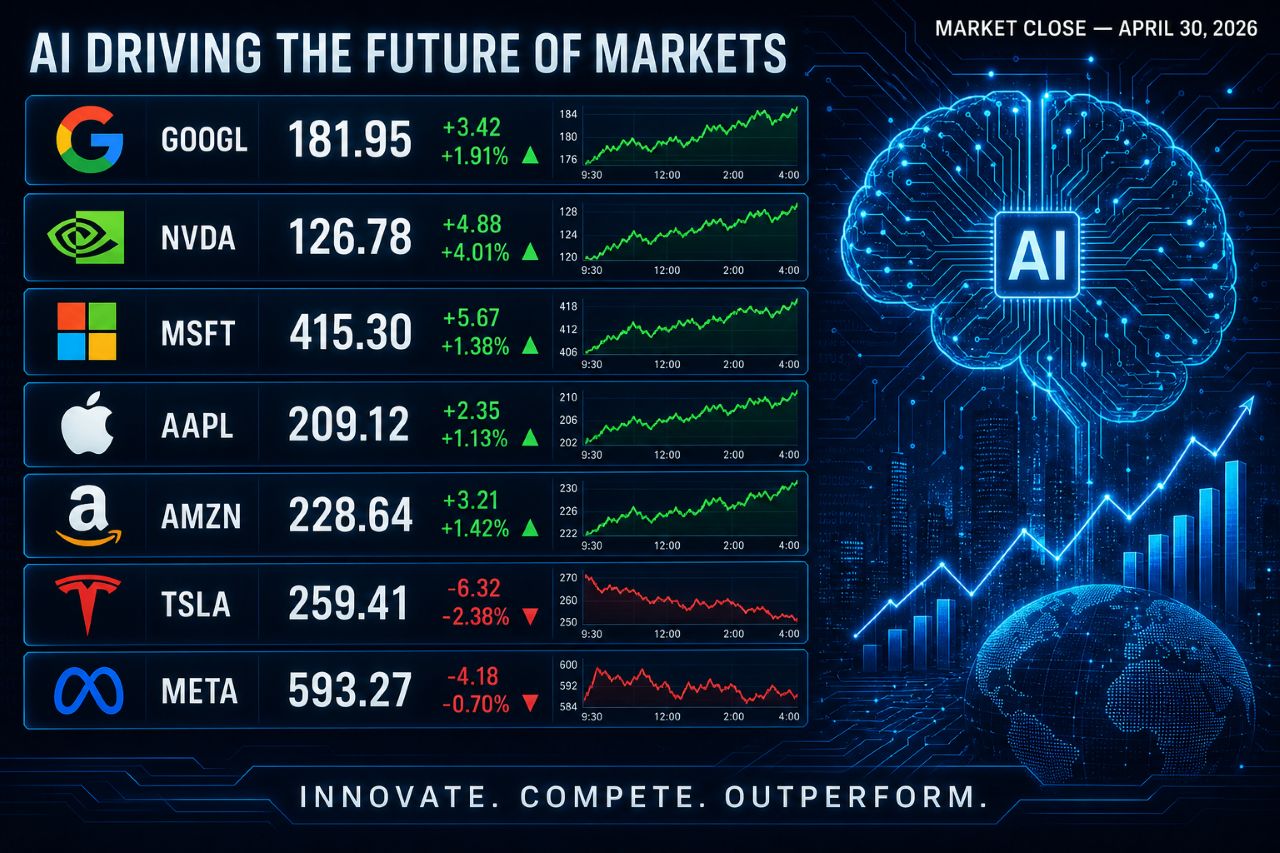

April closed with a thud of cash registers and a sharp sorting of the Big Tech bench. By Thursday’s bell on April 30, Wall Street had heard from Alphabet, Amazon, Microsoft, Meta, Apple, Qualcomm and Caterpillar inside roughly 36 hours, and the message coming back from investors was unusually blunt for a quarter where every megacap technically beat the consensus number. Companies that could show AI dollars hitting the top line got bid up. Companies that could only show AI dollars going out the door got marked down. The S&P 500 rode the split to a fresh record close at 7,209.01, up 1.02 percent on the day, while the Nasdaq added 0.89 percent and the Dow tacked on 790 points behind a Caterpillar surge that nobody had on their bingo card a week ago.

The macro frame is simple. Hyperscalers spent a combined record above $130 billion on AI capital expenditures in Q1 alone, and the Street has spent six months tolerating the bill on faith. This week the patience ran out. The earnings tape rewarded proof and punished promise, and the two camps formed in real time.

ALPHABET DELIVERED THE NUMBER WALL STREET WAS WAITING FOR

Alphabet was the trade of the week. Consolidated revenue hit $109.9 billion, up 22 percent year over year, with net income climbing 81 percent and diluted earnings per share at $5.11, an 82 percent jump. The headline that mattered, though, was Google Cloud. Revenue there accelerated 63 percent and crossed $20 billion in a single quarter for the first time, a level that puts Sundar Pichai’s cloud unit on a runrate roughly equal to where AWS sat about four years ago. The stock jumped close to 10 percent on the print, an enormous move for a company of Alphabet’s size, and you could feel the relief radiating out of every long-only fund that had spent two years explaining to clients why the ad business was not a one-trick pony.

What changed the conversation is the mix. Search held up, YouTube held up, and the AI infrastructure unit suddenly looks like a real revenue engine rather than a science project. Pichai’s bet that owning silicon, models, the cloud and the distribution layer would compound into pricing power is, for one quarter at least, paying out exactly the way he sketched it on a slide twelve months ago.

AMAZON SHOWED THE INVOICE AND GOT A PASS

Amazon got the second-cleanest reception. AWS revenue rose 28 percent to $37.6 billion, the kind of growth reacceleration the bears had been telling clients was structurally over, and Andy Jassy used the call to reaffirm the $200 billion AI investment target for the year. That is not a typo. Two hundred billion. The stock still closed up 0.77 percent on Thursday, which doesn’t sound like much until you remember that Amazon also issued cautious operating income guidance and is openly telling the market that capex will keep climbing. Investors swallowed all of it because the cloud number told them the spending is showing up as enterprise contracts. Bloomberg’s read on the bonanza framed it cleanly: the hyperscalers that grew cloud the fastest got the benefit of the doubt on the bill.

Jassy’s pitch is a familiar one for anyone who watched Bezos run the playbook in the 2010s. Spend ahead of demand, lock in capacity, and let competitors try to catch up while you bank multi-year enterprise deals. The risk is that the AI demand curve flattens before the depreciation curve hits. The bull case is that Amazon will be the only company at the scale required when it doesn’t.

APPLE’S RECORD QUARTER LANDED HARD

Apple was the late punctuation. The company posted a Q2 record of $111.2 billion in revenue, up 17 percent year over year, with $29.6 billion in net profit and diluted EPS of $2.01. iPhone revenue alone jumped to $56.99 billion from $46.84 billion a year ago. Tim Cook called the iPhone 17 lineup the most popular in the company’s history and said the quarter beat guidance “despite supply constraints,” which is the kind of sentence that makes operations people on the analyst side stop and rewind. Services revenue climbed about 16 percent to $30.9 billion, gross margin came in at 49.3 percent, and double-digit growth showed up in every product category and every region.

The optics matter. Apple has been the megacap most accused of falling behind on generative AI, and yet it just printed a record quarter on the strength of hardware and an annuity-like services business that nobody is talking about anymore. Whatever Apple’s AI strategy ends up being, the cash flow funding it is fully intact, and Cook bought himself another quarter of runway to get Apple Intelligence and the Siri overhaul shipped without panic in the room.

META AND MICROSOFT GOT THE CAPEX TAX

Now the other side of the ledger. Meta beat on revenue and still fell roughly 8 percent on Thursday. The user numbers came in soft, capital expenditures were below estimates in a way that read as either guidance whiplash or genuine retrenchment, and the AI spending plans for the back half of the year landed with a thump. Microsoft slipped 4 percent on a beat of its own, also for AI capex reasons, even with cloud growth that any normal quarter would have triggered a pop.

The pattern is hard to miss. Investors are no longer giving the same benefit of the doubt to every hyperscaler. They want to see the AI dollar go in, come back out as cloud or ad revenue, and do it inside a window short enough to keep return-on-invested-capital math from breaking. Meta’s case is harder because Reality Labs is still a multi-billion-dollar drag, and any incremental AI spend gets mentally added to the Metaverse line by analysts who are still skeptical Mark Zuckerberg has the discipline to pull back. Microsoft has the cleaner cloud story, but its capex line has gotten so large that even healthy revenue growth is no longer enough to offset the fear of stranded data center capacity if AI demand softens.

CATERPILLAR AND QUALCOMM STOLE A CHUNK OF THE HEADLINES

The two breakout names of the day didn’t even come from the obvious AI bench. Caterpillar popped nearly 10 percent after reporting adjusted EPS of $5.54 on $17.42 billion of revenue, against consensus of $4.65 and $16.53 billion, and raised its annual revenue outlook on top. The construction equipment maker is a back-door AI infrastructure trade. Every hyperscaler data center being built right now needs Cat machines, generators and engines on site. When Caterpillar guides up, it is telling you the physical buildout is real, not just slideware.

Qualcomm was the bigger surprise. The chipmaker reported $10.6 billion in revenue and adjusted EPS of $2.65, beating estimates by nine cents, and CEO Cristiano Amon casually announced on the call that the company will begin shipping data center chips to a “large hyperscaler” inside the calendar year. The stock ripped 15 percent on Thursday. Add in record automotive revenue crossing a $5 billion annualized runrate on the Snapdragon Digital Chassis platform, and Qualcomm just rewrote its own narrative from a handset cyclical to a multi-leg infrastructure story. CNBC’s coverage of the Qualcomm move noted the data center hint and the China handset recovery commentary did most of the heavy lifting on the tape.

THE TAKEAWAY: REVENUE NOW EARNS THE CAPEX

Step back from the individual scoreboard and a single rule fell out of this week’s tape. The market is finally rationing AI capex permission slips. If a company can show cloud, ads, services or hardware acceleration tied to the spending, it gets to keep going. If the only thing on the slide is a bigger capex number for next year, the multiple compresses and the stock takes the hit. Alphabet, Amazon and Apple all delivered something on the revenue side that the Street could underwrite. Meta and Microsoft did not, at least not at a level that justified what they want to spend in 2026.

That is also why Qualcomm and Caterpillar punched through. Both gave investors a clean revenue line attached to the AI infrastructure cycle without asking for tens of billions in new capex first. In a quarter where four hyperscalers reported a combined $130 billion of capital spending, that kind of clarity is worth a re-rating.

Tech stocks are closing out the strongest month since the start of the pandemic in 2020, the indexes are at all-time highs, and the bull case for the year remains intact. But the loudest signal coming out of yesterday’s earnings tape is that investors are starting to price the AI buildout the way they used to price industrial capex cycles. Show the contracts. Show the revenue. Show the return. Faith is no longer enough to fund the next data center.