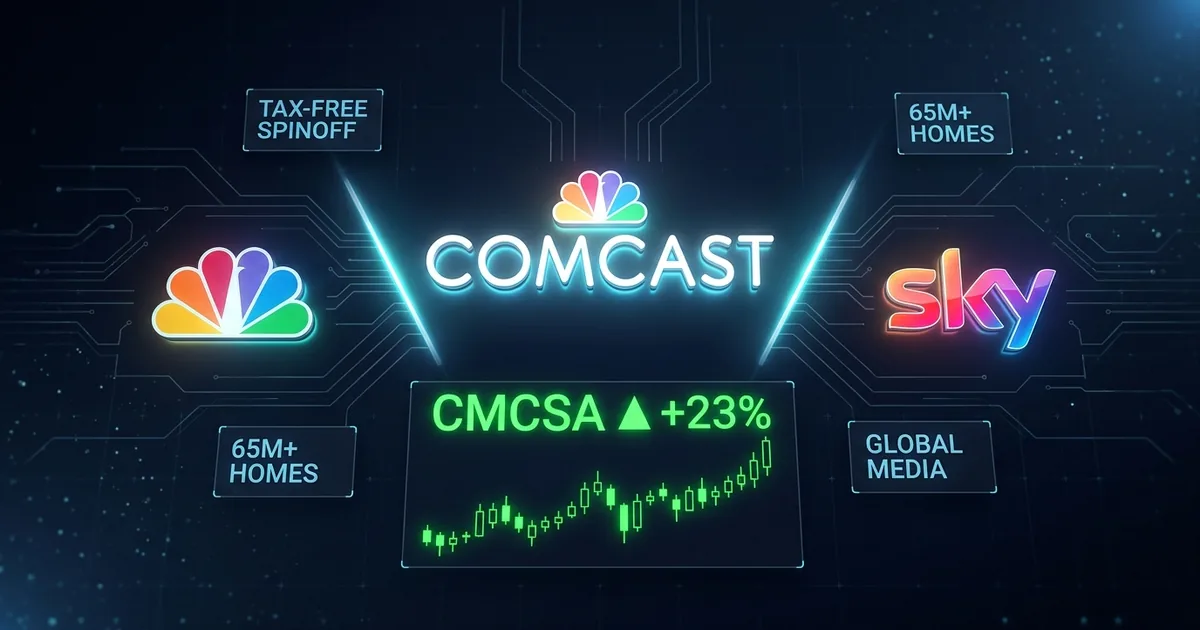

Comcast just told Wall Street what Wall Street has been telling media conglomerates for a decade: these businesses are worth more apart than together. The company’s stock surged as much as 23% after announcing it will spin off NBCUniversal and Sky into a separate publicly traded company, effectively completing a three-way dismantling of what was once America’s most sprawling media-telecom empire.

The Deal Structure Nobody Saw Coming This Fast

The tax-free spinoff will cleave Comcast into two independent entities. The new NBCUniversal company inherits Universal’s film and television studios, the NBC broadcast network, Telemundo, Peacock streaming, Bravo, the theme parks division, and Sky’s European media operations. The remaining Comcast keeps the broadband and wireless infrastructure business serving more than 65 million homes and businesses across the United States.

Mike Cavanagh, currently a top Comcast executive, will run the spun-off NBCUniversal as CEO. Michael Angelakis, a former Comcast chief financial officer, takes over as CEO of the slimmed-down Comcast. The transaction is expected to close within approximately one year, and CNBC reported that shareholders will receive shares in both companies upon completion.

Why the Market Is Paying a 23% Premium for Destruction

The stock reaction tells the whole story. For years, Comcast’s conglomerate structure forced a high-margin broadband cash machine to subsidize the uncertain economics of streaming, content production, and linear TV decline. Investors who wanted exposure to American broadband infrastructure had to swallow Peacock’s subscriber acquisition costs and Sky’s European regulatory headaches. Investors who liked NBCUniversal’s content library and theme park margins had to accept declining cable subscriber counts dragging the multiple down.

That structural tension is exactly what drove Comcast to spin off Versant Media Group in January 2026. Comcast completed that separation effective January 2, sending its cable television networks, including CNBC, MS NOW (formerly MSNBC), USA Network, Syfy, E!, Oxygen, and Golf Channel, into a standalone public company trading on Nasdaq under the ticker VSNT.

Six months later, the second shoe drops. What began as a cable network carve-out has become a full corporate autopsy. Three separate public companies will emerge from what Brian Roberts built over three decades of deal-making: a broadband utility, a studio-and-parks entertainment company, and a cable network portfolio that already trades independently.

The Deconglomeration Wave Is Now a Flood

Comcast is not operating in a vacuum. The entire media industry is unwinding the conglomerate thesis that defined entertainment business strategy from the 1990s through the 2010s. The logic of vertical integration, owning the pipes and the content that flows through them, assumed that bundling would create pricing power and reduce customer acquisition costs. Streaming economics obliterated that thesis. Content costs exploded, subscriber growth plateaued, and the pipes turned out to be the only part of the business with durable margins.

The Paramount-Warner Bros. Discovery merger that cleared the DOJ without concessions earlier this month represents the other side of the same coin. If you cannot sustain a conglomerate, you either break up into focused pieces (Comcast’s path) or merge into a single focused giant (Paramount-WBD’s path). Both moves are admissions that the old model is dead.

Variety reported that the NBCUniversal spinoff will create one of the largest standalone entertainment companies in the world, combining Universal Studios’ film and television production with Peacock’s direct-to-consumer platform and Sky’s 23-million-subscriber European footprint. The theme parks division alone generated billions in operating income last year, making the entertainment company a formidable standalone entity from day one.

What Each Piece Looks Like Standing Alone

The remaining Comcast becomes a pure-play connectivity company. Broadband, wireless, and the Xfinity entertainment platform form a predictable, high-margin business that throws off substantial free cash flow. That profile attracts a completely different investor base than a media conglomerate, one that values dividend growth, share buybacks, and the kind of infrastructure moat that streaming companies can only dream about.

NBCUniversal-Sky becomes a content-and-experiences company with global scale. Universal’s film slate, NBC’s broadcast reach, Peacock’s streaming ambitions, and the theme parks’ pricing power create a portfolio that can compete with Disney and the merged Paramount-WBD on both content production and direct distribution. The European footprint through Sky adds international distribution that neither competitor can match in the near term.

Versant, already trading independently, carries the legacy cable networks. That business faces the steepest secular headwinds of the three, but it also operates at margins that make it a viable standalone company as long as it manages the decline curve carefully.

The Roberts Dynasty Question

The unspoken subtext of this entire restructuring is succession. Brian Roberts has controlled Comcast through a dual-class share structure for decades. Breaking the company into three pieces, each with its own CEO and board, raises the question of how that control apparatus evolves. Neither Cavanagh nor Angelakis is a Roberts family member. The governance of three separate public companies, all descended from one founder’s empire, will be one of the most watched corporate succession stories of the next several years.

For now, the market has rendered its verdict with a 23% premium. The sum of the parts is worth meaningfully more than the whole. That is both a validation of the breakup strategy and an indictment of the conglomerate model that preceded it.