Macy’s just delivered the kind of quarter that makes the “retail is dead” crowd uncomfortable. The department store chain posted 3% comparable sales growth in Q1, its best first-quarter performance since 2022, and raised its full-year guidance across every major metric. In a week where the Nasdaq lost $1.3 trillion, a 165-year-old department store was one of the market’s bright spots.

The Numbers Tell a Clean Story

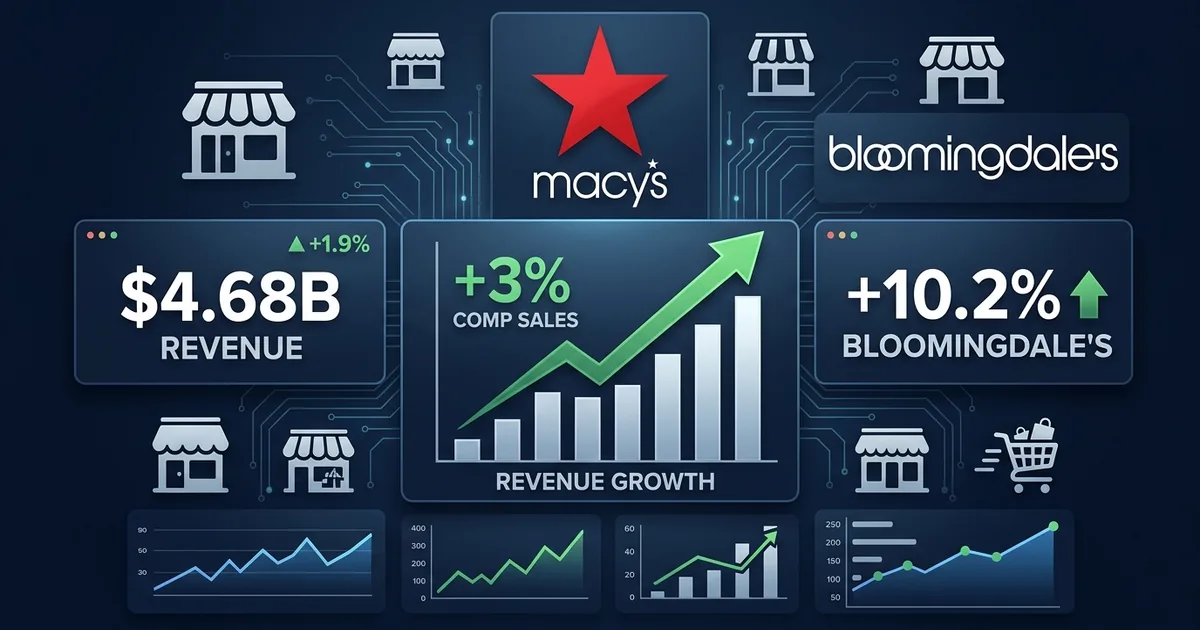

Net sales rose 1.8% to $4.68 billion for the quarter ended May 2. Net income came in at $63 million, or 23 cents per diluted share, beating consensus expectations. Comparable sales growth of 3% was broad-based, not concentrated in a single category or driven by a one-time event.

The standout was Bloomingdale’s. The luxury division posted 10.2% comparable sales growth, a record for its first-quarter results according to Sherwood News. That performance suggests the higher-income consumer remains resilient, even as inflation and interest rate uncertainty weigh on broader sentiment.

Guidance Goes Up, Not Down

Macy’s lifted its full-year net sales forecast to $21.5 billion to $21.75 billion, up from a prior range of $21.4 billion to $21.65 billion. More telling: comparable sales guidance swung from a range of negative 0.5% to positive 0.5% to a new range of positive 0.5% to positive 1.2%. The company is no longer hedging against a decline. It is projecting growth.

Adjusted diluted earnings per share guidance rose to $2.00 to $2.20, from $1.90 to $2.10. The raises were modest in absolute terms but directionally significant. In a macro environment where most consumer-facing companies are guiding cautiously, Macy’s leaned into optimism.

Why This Matters Beyond One Retailer

The results land at an interesting moment for the consumer economy. BigGo Finance tracked the earnings beat and noted the company’s “Bold New Chapter” turnaround strategy as a key driver. The broader question is whether Macy’s is an outlier or an indicator.

Consumer spending data has been mixed. Credit card delinquencies are rising. Student loan payments are back. Inflation has been sticky enough to keep the Fed from cutting rates, and prediction markets now price in a possible hike. Against that backdrop, a department store chain posting its best growth in four years deserves scrutiny.

The answer may be that Macy’s has benefited from precisely the kind of operational discipline that the market has been rewarding: headcount optimization, store fleet rationalization, and a focus on higher-margin private label brands. The company closed underperforming locations, invested in its digital platform, and leaned into the Bloomingdale’s and Bluemercury brands where average transaction values are higher.

The Brick-and-Mortar Counternarrative

For years, the conventional wisdom held that physical retail was a secular loser. Amazon and e-commerce would eat everything. But the data has been telling a more nuanced story. Consumers still want to touch luxury goods before buying them. Experiential retail, personalized service, and curated assortments have a place in a world of infinite digital choice.

Macy’s Q1 results support this counternarrative. Same-store sales growth of 3% is not a dead category’s number. It is a turnaround story gaining momentum alongside other traditional retailers like Home Depot that have also surprised to the upside this quarter.

What Comes Next

The risk for Macy’s is the same risk facing every consumer-facing company: if the Fed actually hikes rates, disposable income gets squeezed further. Mortgage rates stay elevated. Auto loan costs climb. The marginal consumer who drove Macy’s Q1 outperformance may pull back.

But for now, the numbers are the numbers. A 3% comp, a guidance raise, and a luxury division setting records. The market rewarded the stock accordingly. Sometimes the boring business in the boring sector is the one quietly compounding while everyone else chases AI.