Tesla beat on earnings. Tesla missed on deliveries. Tesla raised capital spending by $5 billion. Welcome to 2026, where the world’s most expensive car company just admitted it wants to be something else entirely.

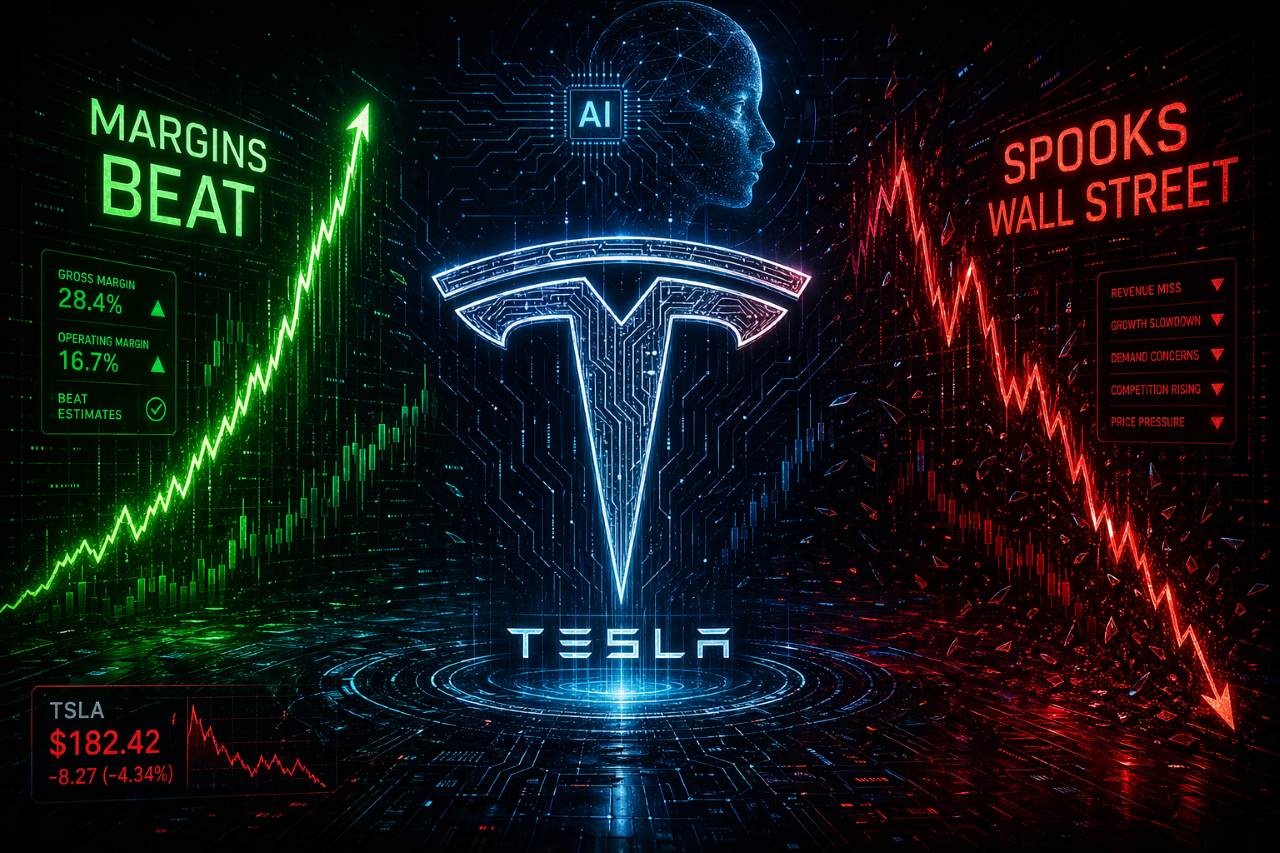

The first quarter numbers look deceptively normal on the surface: adjusted earnings per share of $0.41 crushed expectations of $0.37, net income came in at $1.45 billion versus a consensus of $1.17 billion, and the stock initially jumped 4 percent in after-hours trading. But if you blinked during the earnings call, you missed the real story. Elon Musk didn’t spend that airtime talking about the 358,023 vehicles Tesla delivered (a shortfall that matters) or the revenue miss of $22.39 billion against a $22.64 billion estimate. He talked about artificial intelligence. He talked about chips. He talked about a $25 billion capex plan that makes the company’s traditional auto business look like a side hustle.

That $25 billion number wiped out the stock’s gains by market close. And it should have. Because Tesla just signaled something profound: the car business is no longer the point.

The Margin Story Nobody Expected

Let’s start with what actually impressed Wall Street before the pivot. Tesla’s gross margin hit 21.1 percent, a number that seemed nearly impossible given the pricing environment. Consensus was calling for 17.5 percent. The difference between those two lines isn’t accounting; it’s strategy.

For years, Tesla’s margin story was about scale. Build more cars, cut costs, profit margins expand. That’s the playbook every automaker runs. But something shifted. Tesla’s pricing power in energy storage is real. Its manufacturing efficiency continues to improve. And more importantly, the company is starting to harvest the accumulated intellectual property from its power business. That 21.1 percent gross margin reveals a company that has finally figured out how to make money outside the vehicle sale itself.

Here’s the problem: nobody wants to talk about that, because everyone is too busy asking why vehicle deliveries missed by 7,600 units and why energy storage deployment fell 38 percent sequentially to just 8.8 GWh.

The California Question and the Delivery Gap

Tesla’s delivery miss isn’t a rounding error. It’s evidence that California registrations are plunging, that the EV market is starting to sober up after years of euphoria, and that competition is finally arriving. The company faced serious headwinds in Q1. Incentives shrunk. Federal tax credits started to feel less generous. New competition from established automakers landed harder than anyone expected. And Tesla, somehow, still managed to miss delivery targets despite having the brand equity and infrastructure to dominate.

The energy storage miss is worse because it suggests demand isn’t where Tesla thought it was. The company was guiding for 12 to 14 gigawatt-hours deployed annually. It delivered 8.8 GWh in Q1. That’s not a quarterly softness you can blame on timing. That’s a demand crater.

And Musk’s response? Spend $25 billion on AI and manufacturing infrastructure that has almost nothing to do with the vehicles nobody’s ordering.

The $25 Billion Gamble That Changes Everything

This is where the conversation gets interesting. Tesla is raising capex by $5 billion over prior guidance. Some of that goes to traditional manufacturing expansion. Some goes to energy storage factories. But the biggest chunk goes to AI infrastructure, chip design, and computing power that will allegedly power Tesla’s robotics and autonomous vehicle ambitions.

The market hated it. And the market was right to hate it, not because the spending is irresponsible, but because it reveals a fundamental reality Musk has been dancing around for two years: Tesla is betting that the future of the company is in autonomous systems and robotics, not in selling vehicles to regular people.

Think about what that means. A company that built its brand on selling electric cars is now asking shareholders to fund a moonshot in AI computing while its core business is contracting. Deliveries are missing. Energy storage demand is softer than expected. And the response is to spend $25 billion on speculative infrastructure that probably won’t generate revenue at meaningful scale before 2028 or later.

Musk’s tone on the call reflected this reality. He talked about costs ahead. He acknowledged that the business is facing pressure. He didn’t project confident margin expansion or delivery growth in the near term. What he did was ask for patience and faith that the AI bet would eventually justify the spend.

Is Tesla a Car Company or an AI Company? It’s Now a $25 Billion Question

This is the fundamental tension that the Q1 earnings revealed. Tesla has always been positioned as a vehicle manufacturer with software expertise. The stock gets valued on a multiple that assumes it’s going to build millions of cars at improving margins. Wall Street analysts model the business as a mature automotive OEM with better technology.

But the $25 billion capex guidance suggests Tesla’s management doesn’t actually believe that story anymore. Or maybe they never did, and we’ve been naive.

The problem with being a car company is that you’re competing with Toyota, BMW, and Volkswagen. It’s brutal. Margins are permanently under pressure. You have to keep delivering. You have to keep innovating just to maintain market share. It’s a competent business if you’re good at it, but it’s not a home run.

The problem with being an AI company is that you’re competing with Nvidia, Google, and eventually OpenAI. You’re building infrastructure that everyone else will eventually duplicate or exceed. But the narrative is better. The potential returns are theoretically infinite. And if you can convince your shareholders that you’re actually a chip and robotics company wearing a Tesla badge, you get valued on a venture capital multiple instead of an automotive multiple.

Guess which story Wall Street prefers to believe?

What Happens Next

Tesla’s gross margin beat is real and important. The company has figured out how to make more money per vehicle and per megawatt-hour of storage. That’s a genuine operational achievement. But it’s not enough to offset the fact that deliveries are missing and demand isn’t where the company needs it to be.

The $25 billion capex plan is a bet. A big one. It assumes that autonomous vehicles and humanoid robots are coming faster than most people think. It assumes that Tesla can build AI infrastructure faster and cheaper than companies that are actually specialized in AI. It assumes that the car business can run on lower margins while the company invests in speculative bets that might not pay off for years.

That’s not a strategy. That’s a hope. And on Wall Street, hope is fine as long as you’re executing. The moment execution stumbles, hope becomes scary.

Tesla delivered good margins and bad deliveries. It printed more profit from fewer sales. And then it told investors it wanted to spend $25 billion becoming something completely different. That’s not earnings stability. That’s a company in transition, betting everything on a pivot.

The stock initially believed the earnings. It immediately doubted the capex. That’s probably the right instinct.

See Bloomberg’s analysis of Tesla’s Q1 performance and CNBC’s deeper dive into the capex implications for more context on how these numbers fit into Tesla’s broader strategy.