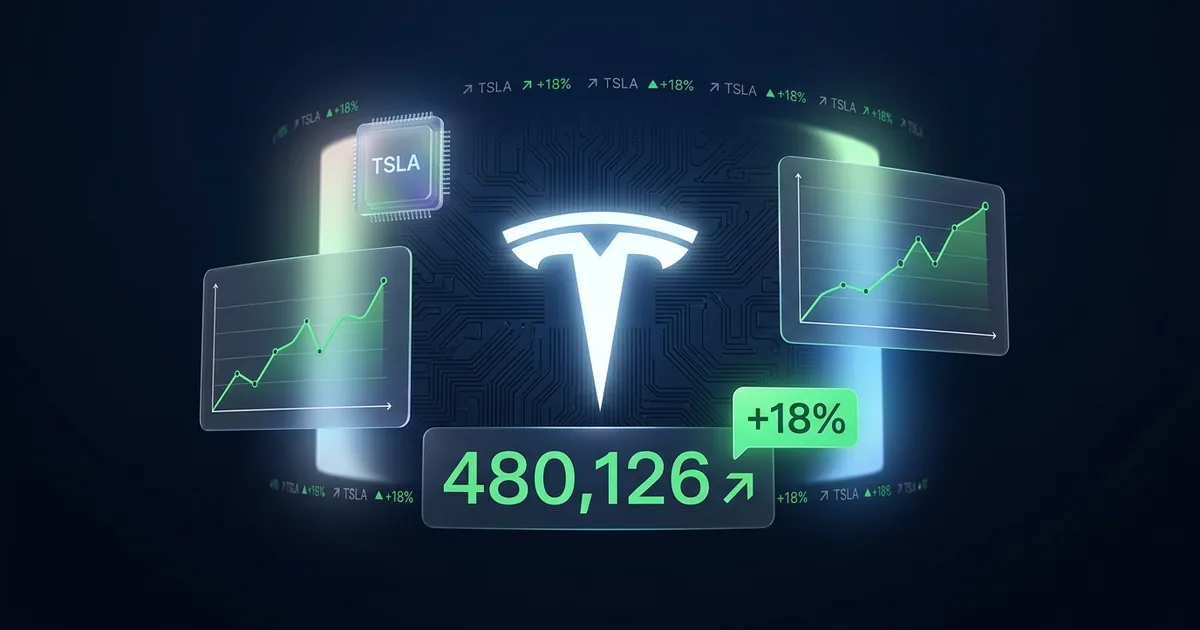

Tesla just posted its strongest quarterly delivery number since the sales slump began, and it wasn’t close. The company reported 480,126 vehicle deliveries for Q2 2026, blowing past the 406,024-unit Wall Street consensus by roughly 74,000 vehicles. That is an 18% beat on the most closely watched metric in the EV industry, and it reframes the demand-recovery debate heading into earnings on July 22.

The structural story is not just that Tesla sold more cars. It is where the cars went. International markets, Europe in particular, drove the outperformance while U.S. sales continued to decline. Tesla is hedging its domestic brand-risk problem with geographic diversification, and this quarter proved the strategy works at scale.

The Numbers Behind the Beat

Tesla produced 451,758 vehicles and delivered 480,126 in the quarter, drawing down inventory built during Q1’s weaker period. The Model 3 and Model Y accounted for 467,762 of those deliveries, with the remaining 12,364 units spread across Cybertruck, Model S, Model X, and Semi.

Sequential growth was staggering. Q1 2026 deliveries came in at 358,023 vehicles, making Q2’s result a 34% jump quarter over quarter. Year over year, the gain was approximately 25%, since Q2 2025 landed near 384,000 units.

Goldman Sachs had raised its Q2 estimate to 420,000 vehicles ahead of the print, citing stronger-than-expected European registrations. Even that bullish revision fell 60,000 units short. Bloomberg’s consensus sat lower still at 397,000.

The energy storage business added another data point: 13.5 GWh deployed in Q2, continuing a growth trajectory that Tesla has been quietly building into a second revenue pillar.

Why This Beat Matters More Than the Number Suggests

The significance extends beyond the delivery count. Tesla entered 2026 under a cloud of compounding headwinds: Elon Musk’s polarizing political activities had damaged the brand domestically, federal EV tax credits expired at the end of 2025, and BYD was on pace to deliver 557,000 battery-electric vehicles in Q2 to Tesla’s 480,000. The “Tesla is dying” narrative had institutional weight behind it.

This print does not eliminate those problems, but it dismantles the thesis that demand is in structural decline. The mechanism is geographic arbitrage. While American consumers who associate Tesla with Musk’s politics have pulled back, European and Asian buyers have not. Tesla’s ability to redirect production and marketing spend toward healthier markets is the operational capability the bears underestimated.

The timing matters too. TSLA shares entered the report at roughly $425, already up 24% from the April low, according to TradingKey’s pre-report analysis. A beat of this magnitude on the single metric investors watch most closely gives the stock a fundamental catalyst it has lacked since the robotaxi hype cycle cooled. The company’s Dallas robotaxi pilot remains in safety validation mode, which means the delivery number is doing the heavy lifting on its own.

The BYD Comparison and What It Reveals

BYD’s 557,000 battery-electric deliveries still top Tesla’s 480,000, but the gap narrowed meaningfully this quarter. More importantly, the two companies are fighting on different fronts. BYD dominates on price in China and Southeast Asia. Tesla’s margin recovery depends on premium positioning and software-attached revenue in Western markets.

The competitive dynamic is shifting from a zero-sum race to a market-segmentation story. Both companies are growing, which means the overall EV demand pool is expanding, not just redistributing. That is a more constructive macro read than the “BYD is eating Tesla alive” framing that dominated Q1 coverage.

What to Watch on July 22

The delivery number sets the table. The earnings call on July 22 will reveal whether the volume translated into margin improvement or was bought with incentives. Three questions will define the print:

First, gross margins on the auto segment. If Tesla sold 480,000 vehicles at improving margins, the revenue and profit beat will compound. If it took aggressive discounting to hit the number, the story flips from demand recovery to margin compression.

Second, the geographic revenue split. Investors will want granularity on which markets drove the upside and whether that mix is sustainable or was pulled forward by one-time factors like European subsidy deadlines.

Third, guidance. Tesla has been cagey about forward numbers. A raised full-year delivery target, even a modest one, would confirm that management sees the Q2 strength as durable rather than a seasonal blip.

For now, the delivery print speaks for itself. Tesla’s demand problem was real, but 480,000 vehicles in a single quarter is not what structural decline looks like. The bears will need a new thesis.