The semiconductor trade that defined the first half of 2026 is getting a violent correction. Samsung Electronics and SK Hynix shares crashed more than 7% on the Korea Exchange Thursday morning, extending a selloff that started on Wall Street when investors began dumping chip stocks after an 80% to 100% rally in the sector over the past six months.

What Triggered the Unwind

The trigger was straightforward profit-taking, but the scale was anything but ordinary. Micron Technology dropped more than 10% on Wednesday, its steepest single-day decline in months, despite the company still sitting on a 260% year-to-date gain. AMD, Intel, and most of the Philadelphia Semiconductor Index followed Micron lower, with the SOX index declining more than 5% in a single session.

The selling accelerated after Fed Chair Kevin Warsh struck a hawkish tone at the ECB Forum in Sintra, Portugal, telling the audience that inflation remains “too high” and declining to signal relief on interest rates before the next Federal Open Market Committee meeting. For a sector that had priced in an almost infinite AI demand runway, even a whiff of tighter-for-longer monetary policy was enough to trigger the exit.

Asia Got Hit Harder

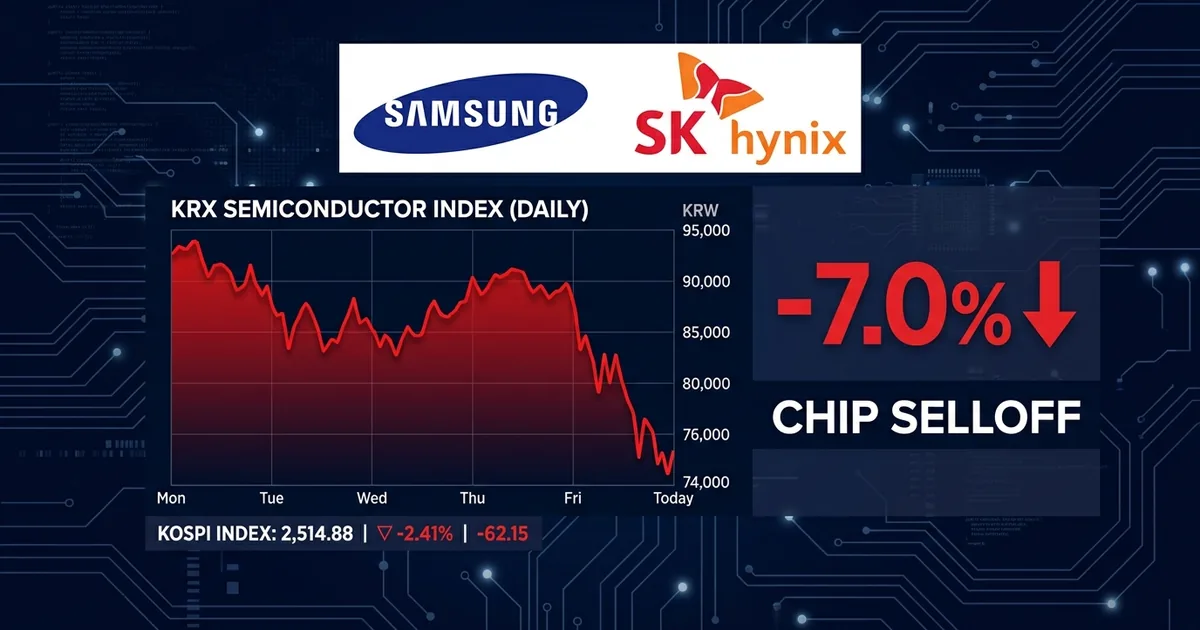

The KOSPI tech selloff Thursday was amplified by the outsized weight Samsung and SK Hynix carry in South Korea’s benchmark index. Samsung fell 7.2% and SK Hynix dropped 7.8%, erasing tens of billions in market capitalization in a matter of hours. The damage spread across Asia, with Tokyo Electron, TSMC’s Taipei-listed shares, and other regional semiconductor names all trading sharply lower.

South Korea’s semiconductor sector is particularly exposed because the government just announced a 576 trillion won ($420 billion) national strategy to dominate AI chip manufacturing and next-generation memory. That policy bet looks prescient over a five-year horizon but creates short-term vulnerability: when global investors rotate out of semiconductors, Korean equities take a disproportionate hit because the sector makes up roughly 30% of the KOSPI’s total market capitalization.

The Crowded Trade Problem

What makes this correction different from routine sector volatility is the degree of concentration. Semiconductor stocks became the most crowded institutional trade of 2026, with AI demand narratives pulling in everything from passive index flows to momentum-chasing hedge funds. The Philadelphia Semiconductor Index gained roughly 95% in the first half of the year, a pace that historically precedes a mean-reversion move of 15% to 25%.

The Nasdaq Composite declined 0.66% to 26,040.03 on Wednesday, with the S&P 500 falling 0.22% to 7,483.23. Those headline numbers masked the severity of the semiconductor selloff because mega-cap tech names like Apple and Microsoft held relatively steady, offsetting the chip losses at the index level.

Is This a Correction or a Reversal?

The consensus among analysts remains that this is a healthy correction within a secular bull trend, not the beginning of a reversal. AI infrastructure spending continues to accelerate: Bloom Energy and Brookfield just expanded their data center power partnership to $25 billion, and KKR’s Helix Digital Infrastructure launched with $10 billion in committed capital. The demand signal for GPUs, high-bandwidth memory, and advanced packaging has not weakened.

But the price action matters. Micron trading at 260% above its January levels created a setup where even moderately disappointing guidance or a hawkish Fed data point could trigger violent position unwinding. That is exactly what happened Wednesday, and the question now is whether the dip buyers who have stepped in at every previous selloff will show up again before the June jobs report drops at 8:30 a.m. Eastern.

The jobs number matters because a weak print would bolster the case for a rate pause, which would be positive for growth stocks including semiconductors. A strong print would reinforce Warsh’s hawkish stance and could extend the selloff into a second day. Either way, the chip trade is no longer the one-way bet it was in Q1. The AI thesis is intact, but the easy money has already been made.