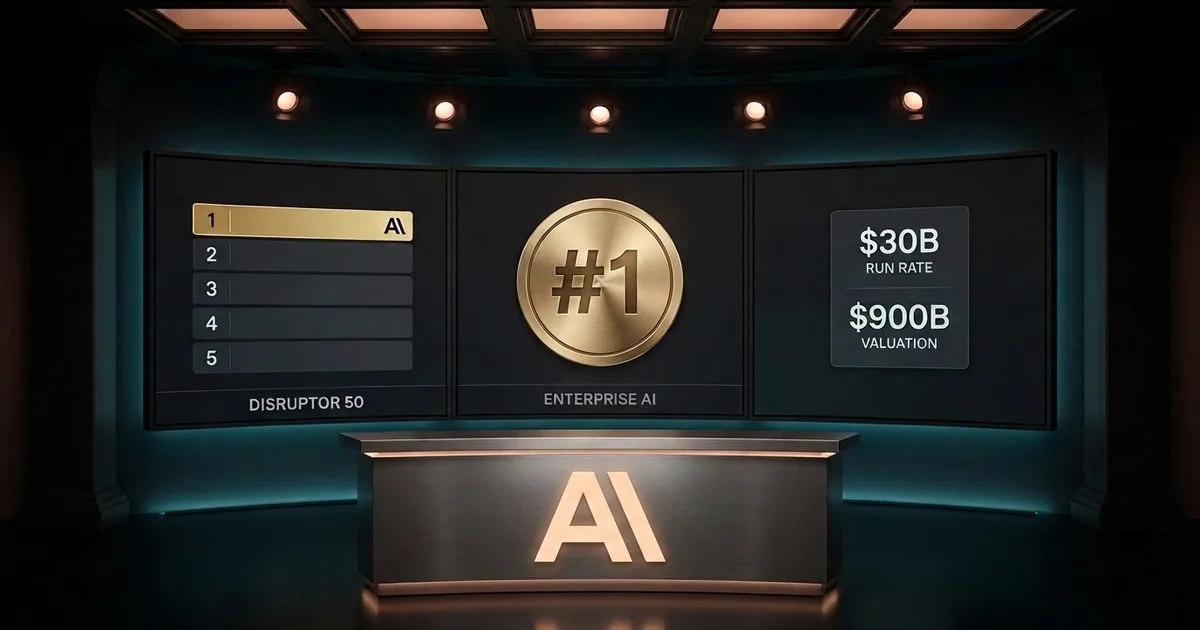

CNBC published its 2026 Disruptor 50 list this morning, and Anthropic is the new number one. The company jumped three spots from #4 last year and, in doing so, became the first AI lab to formally displace OpenAI on a major business-press ranking. The numbers behind the move are not subtle. CEO Dario Amodei told CNBC that Q1 revenue grew 80 times year over year. The annualized revenue run rate has climbed past $30 billion, up from $9 billion at the end of 2025. And the in-flight Series F discussions point to a valuation north of $900 billion, which would make Anthropic worth more than OpenAI on paper for the first time since the rivalry began.

Rankings are usually vanity. This one is not. The Disruptor 50 has historically been the magazine-cover moment that institutional allocators read on the morning treadmill and that strategic acquirers cite in board memos. When Uber topped the list in 2014, it preceded the megaround that took it to $40 billion. When ByteDance topped it in 2020, that was the public marker of the moment TikTok became the most important platform in the world. Anthropic getting the slot in 2026 is the press establishment formally adjusting the AI pecking order in front of every Fortune 500 CIO.

How Claude Code Quietly Became The Enterprise Default

The single most important Anthropic product nobody outside the developer community fully appreciates yet is Claude Code. According to Anthropic’s Series F announcement, Claude Code is already generating over $500 million in run-rate revenue eight months after general availability, with usage growing more than 10x in three months. That is the fastest ramp ever recorded for an enterprise developer tool. It is faster than GitHub’s early years, faster than Datadog at the equivalent stage, faster than Snowflake’s enterprise expansion arc.

The reason it matters is structural. Coding is the highest-value, highest-friction workflow inside every enterprise IT budget. If you win the developer surface, you win the data, the tooling, the workflow, and eventually the agent layer that automates the rest of the back office. We laid out the full strategic frame in our deeper look at how Claude Code flipped the enterprise AI market and cracked the OpenAI IPO story. The Disruptor 50 ranking is the public confirmation of what enterprise software analysts have been writing internally for two months: the inflection point happened, and OpenAI did not stop it.

The Revenue Math That Forced The Ranking Change

Look at the raw numbers and the editorial decision becomes obvious. Anthropic exited 2025 at roughly $9 billion in annualized revenue. Q1 2026 revenue grew 80x year over year, per Amodei. The current annualized run rate is north of $30 billion. OpenAI’s most recently disclosed run rate, from its January 2026 update, was approximately $25 billion, with reported losses of $14 billion for the trailing twelve months. OpenAI is still the bigger consumer brand. Anthropic is now the bigger enterprise revenue engine, with a meaningfully different cost structure because it does not carry the consumer ChatGPT loss leader.

That delta is what changed the Disruptor 50 calculus. CNBC’s methodology weights revenue scale, growth rate, and disruptive impact on incumbents. Anthropic now leads on all three. Per CNBC’s own breakdown of why Anthropic won the top spot, the editorial team explicitly cited Claude Code as the disruptive lever that separated Anthropic from the rest of the AI cohort. Sierra at #6, OpenAI further down the list, and the appearance of Cerebras and Carbon Robotics in the top 25 round out the AI-heavy 2026 class.

The $900 Billion Valuation Is The Other Story

While the Disruptor 50 ranking was being finalized, Anthropic’s in-flight Series G discussions were doing more financial damage to the OpenAI narrative. Bloomberg reported last week that Anthropic is in early talks to raise at least $30 billion in fresh financing at a valuation of more than $900 billion. No term sheet is signed yet, but the lead investors are reportedly the same sovereign wealth, growth-equity, and crossover hedge funds that have anchored every major AI round of the past two years. If the deal closes at $900 billion, Anthropic surpasses OpenAI’s last reported $300 billion-plus valuation and becomes the most valuable private company in history.

The math, importantly, is not crazy. At a $30 billion run rate growing 80x year over year, $900 billion represents roughly 30 times forward revenue. That is rich, but it is in line with Snowflake’s IPO multiple and below NVIDIA’s current forward multiple. The bear case is that Anthropic’s revenue is concentrated in a small number of large enterprise contracts that could shift if Gemini Omni from today’s Google I/O keynote actually closes the gap. The bull case is that enterprise AI is the largest software replacement cycle in three decades and Anthropic just got named the category leader by the trade press.

What This Does To The OpenAI IPO Math

OpenAI’s path to a 2027 IPO got measurably harder this morning. The CFO Sarah Friar warning two weeks ago about compute capacity was already a flag. Getting publicly outranked on the highest-profile disruptor list in business media is a flag of a different kind. The narrative IPO investors will buy is the one where OpenAI is the dominant pure-play AI platform with the largest moat. That narrative just took a hit, not because OpenAI’s underlying business broke, but because the second-place story is now being told as the leadership story.

Sam Altman’s response will matter more than the ranking itself. Watch for three things. Whether OpenAI accelerates an enterprise-tier announcement to reclaim the developer narrative. Whether the in-flight OpenAI funding talks move faster to lock in a higher private valuation before the IPO window opens. And whether Microsoft, OpenAI’s largest backer and the company with the most to lose if Anthropic’s enterprise lead compounds, makes any visible strategic adjustment in its own AI roadmap.

The Strategic Implications For Every Other AI Company

For the rest of the AI cohort, the Anthropic-at-number-one signal is brutal but clarifying. Enterprise revenue is now the scoreboard. Consumer DAU charts, benchmark wins, and chatbot demo videos no longer move the rankings. The companies that are most exposed to this shift are the ones that have been chasing scale on the consumer side without a comparable enterprise pipeline. Perplexity, Character AI, and the long tail of consumer-facing wrappers are not playing the game that just got named.

The companies that benefit are the picks-and-shovels infrastructure providers. NVIDIA still sits at the bottom of the stack. Snowflake, Databricks, and the data plane vendors all get tailwinds from enterprise AI scale. Sierra, sitting at #6 on the same Disruptor 50 list with its $950 million Series E and $15.8 billion valuation, is the parallel case study: enterprise AI agents are the highest-leverage application layer, and the customer logos are picking quickly.

The Read Forward

Anthropic at number one is the kind of business-press moment that gets quoted in every enterprise procurement deck for the next twelve months. CIOs who were hedging between Claude and ChatGPT now have cover to standardize on Claude. Hedge funds with AI baskets have a fresh ranking to point at. And the Series G discussions just got a measurable boost in fundraising leverage. None of this is permanent. Google could change the picture this afternoon at I/O. Nvidia’s earnings tomorrow could reset the cost-of-compute conversation. OpenAI could ship a product announcement this week that reclaims the headline.

But for one news cycle, the AI hierarchy got rewritten in public, by a publication that no enterprise CIO ignores. Dario Amodei and Daniela Amodei spent five years building the company on the bet that enterprise-grade safety, strong developer tooling, and disciplined commercial execution would beat the consumer brand and the bigger compute war chest. This morning, the trade press agreed. The valuation will follow.