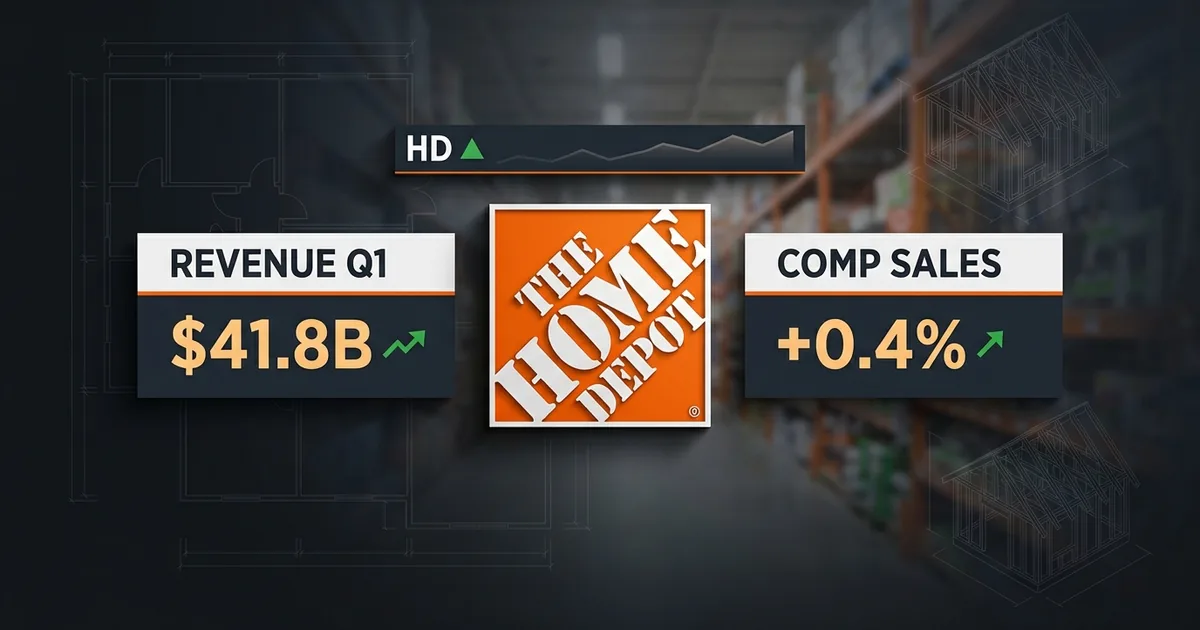

Home Depot just gave Wall Street the cleanest read on the US consumer it is going to get this quarter, and the verdict was better than anyone selling housing-recession trades wanted to hear. Q1 fiscal 2026 sales hit $41.8 billion, up 4.8% year over year and ahead of the $41.59 billion consensus. Adjusted EPS of $3.43 beat the $3.41 Street estimate. US comparable sales rose 0.4%, the first positive print after four straight quarters of declines. And the company reaffirmed full-year guidance of 2.5% to 4.5% sales growth and approximately flat to 2% comparable sales growth. Shares were indicated higher in premarket trade.

Net earnings fell to $3.3 billion from $3.4 billion a year ago, with adjusted EPS down from $3.56, so this is not a triumphant print. It is a print that says the housing-and-pro-contractor side of America is holding together while 30-year mortgage rates back up toward 8% and the long bond rips to 19-year highs. For a market that has been pricing in a consumer crack since February, that is enough to move the stock.

The Comp Sales Inflection Nobody Was Modeling

Comparable sales for the quarter rose 0.6% globally, with US comps up 0.4%. That breaks a streak of four consecutive quarters of negative US comps, the longest run since the 2008-2009 housing collapse. The reason it matters: comps are the single cleanest indicator of organic demand, stripping out new store openings and acquisitions. Going positive in Q1, the historically weakest quarter of the year and the one most exposed to weather, says the underlying demand engine is healthier than the headline economic data implies.

According to Home Depot’s official Q1 release, the strength came primarily from the professional contractor segment, where the company has spent the past two years investing in delivery infrastructure, B2B credit, and the SRS Distribution acquisition. Pro sales outpaced DIY by a comfortable margin, mirroring what Sherwin-Williams and Lowe’s have been signaling all year. The translation: homeowners are still hiring out the bigger projects, even with rates this high.

The Real Story Is What Reaffirmed Guidance Means

Holding the full-year outlook in May 2026 is the most aggressive thing Home Depot’s CFO Richard McPhail could have done. Walk through what has changed since they set the guide in February. The 30-year mortgage rate is back near 7.9% after the bond market sell-off. April CPI came in at 3.8%, hotter than expected. Oil is above $100 a barrel. Consumer confidence hit a multi-year low in March. And the Federal Reserve is now being openly questioned on whether it needs to hike again under new chair Kevin Warsh.

In that environment, the easy executive move is to widen the guidance range, blame macro, and reset expectations to give yourself a buffer for the back half. Home Depot did not do that. The signal is twofold: management has visibility into Q2 backlog, and the pro contractor pipeline is committed enough that they are willing to defend the number publicly. According to Washington Times coverage of the print, executives specifically called out homeowner spring buying patterns and professional spending as the drivers behind their decision to hold guidance.

What This Tells Us About The Other Retailers Reporting This Week

Lowe’s reports Wednesday morning. Target follows after the close. Walmart prints Thursday. Home Depot historically sets the floor for the housing-adjacent retail trade because its mix is the most discretionary and the most rate-sensitive. A positive comp here makes it harder for Lowe’s to disappoint and easier for Target and Walmart to talk constructively about staples. It also raises the bar: if Home Depot can post positive comps with rates this high, Lowe’s investors will not accept “tough macro” as a Q1 excuse.

The bigger lesson is that the US consumer narrative needs more nuance than recession-or-not. The high-income homeowner with a 3% locked-in mortgage and a project list is not the same consumer as the renter facing a 9% APR on a credit card balance. Home Depot is reading the first cohort. Walmart and Target read the second. Both can be true at the same time, and Q1 2026 may be the quarter that proves the divergence has actually widened, not closed.

The Macro Squeeze Hiding Inside The Beat

Look closer at the margin line. Operating margin contracted versus last year, EPS dropped 4.3% on a GAAP basis, and net earnings declined to $3.3 billion from $3.4 billion. Home Depot beat consensus while shrinking its profit pool. Some of that is the SRS Distribution integration, which carries lower contribution margins by design. Some is wage inflation in the distribution network. Some is the cost of holding price on building materials when wholesale prices have moved against them. The takeaway: top-line resilience is real, but it is coming at a cost.

This connects to the macro story we have been tracking all week. The 30-year Treasury yield punched through 5.18% on Tuesday, and our full breakdown of how bond yields are forcing markets to price in a Fed rate hike by March is required reading for understanding why even a guidance reaffirmation cannot fully insulate HD from multiple compression. Home Depot trades at roughly 23 times forward earnings. With long rates rising and earnings flat-to-down, the math gets harder, not easier, even when the operating story is fine.

The Pro Customer Is The Whole Thesis Now

If you are buying Home Depot at these levels, you are buying the pro customer thesis. The DIY consumer is interest-rate sensitive, project-deferral prone, and weighted toward weekend warriors who will skip the deck stain if the credit card balance is uncomfortable. The pro contractor is paid by homeowners who have already decided to do the project, who are funding it from savings or a HELOC at 9% rather than a new purchase mortgage at 8%, and who are tied into multi-month commitments that do not flex with weekly headlines.

SRS Distribution, which Home Depot bought for $18 billion in 2024, is the explicit bet on this thesis. So is the company’s investment in commercial pro fulfillment, in B2B credit products, and in same-day delivery from local distribution centers. Q1 2026 is the first quarter where you can see that strategy producing measurable comp lift. It is also the quarter where the rest of the retail sector will start asking why their own pro initiatives are underperforming.

The Read For The Rest Of The Year

Home Depot just told the market three things. The pro contractor pipeline is real and growing. Q1 was strong enough to defend the full year. And the company is willing to accept margin compression to defend top-line growth and market share through a rate cycle. None of that solves the housing affordability crisis. None of it brings the 30-year mortgage back below 6%. But it does buy management another two quarters of credibility, and it gives the market one less reason to assume the consumer is breaking.

Watch Lowe’s tomorrow for confirmation or contradiction. Watch the housing data prints Thursday for the bigger picture. And watch what Walmart says about lower-income shoppers, because that is where the actual recession risk lives. Home Depot’s quarter is the high-end of the consumer story. The full picture takes two more days to develop.